The purpose of the initiative is to enable companies to begin reporting on a more consistent and comparable manner and catalyse faster progress toward a more formal, systemic solution such as a set of international generally accepted accounting standards for ESG and long-term value considerations. Addressing ESG metrics within an annual report, whether in MD&A, a strategic report, or an integrated report, will ensure material issues are being considered by the board and part of the overall governance process.

Three key concepts addressed in the report include dynamic materiality, “disclose or explain,” and stakeholder capitalism.

Stakeholder capitalism reflects the expectation that the role of business in our contemporary society is to create value over the long-term for the benefit of not only shareholders, but for a wider range of stakeholders, including customers, employees, suppliers and communities.

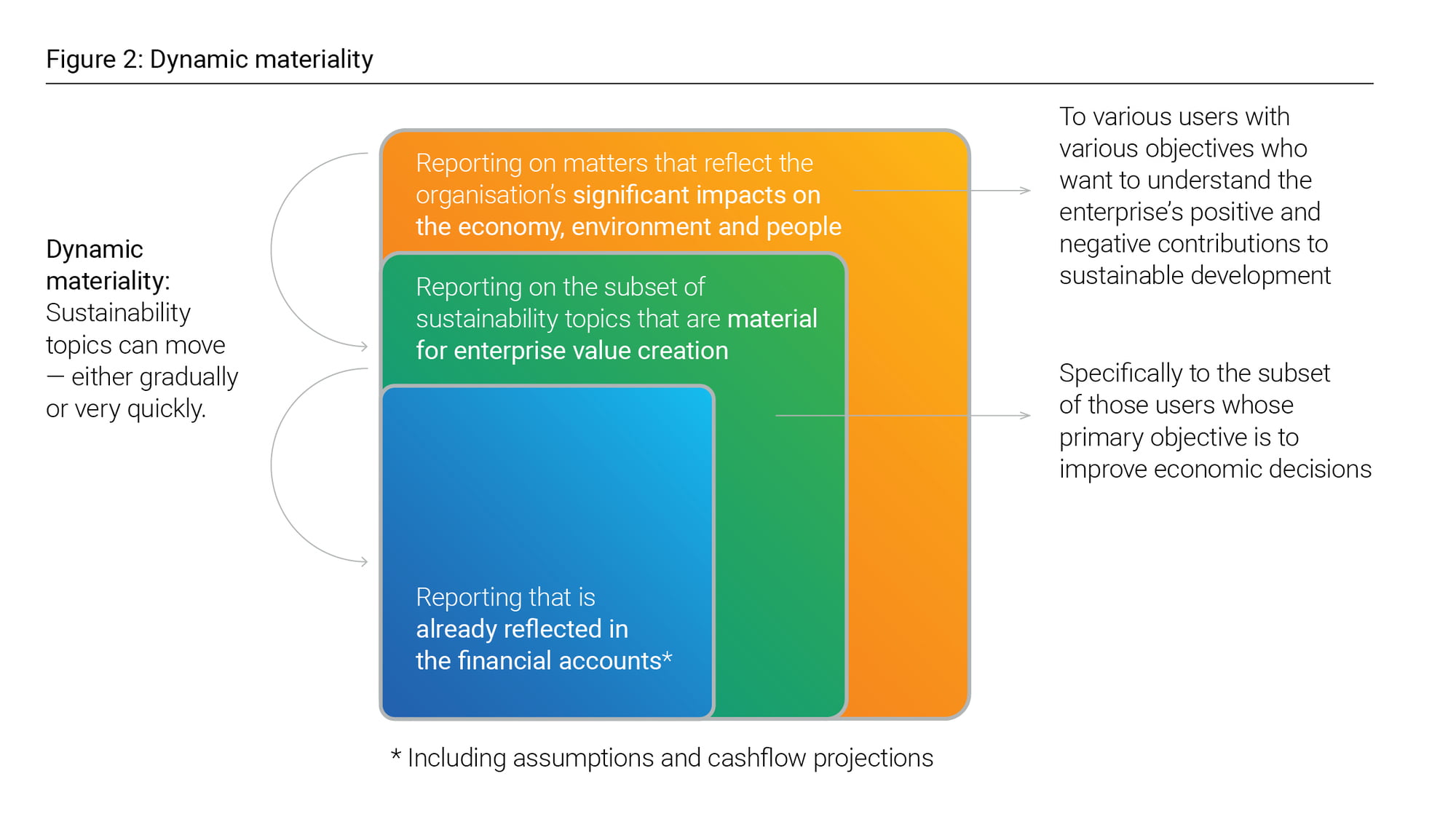

The notion of dynamic materiality as depicted by Figure 2 (excerpted in the report from the noted Statement of Intent5), addresses the possibility that sustainability topics can move between the set of topics that are material for the broader stakeholder audience interested in sustainable development, and the sub-set of topics that are material for enterprise value creation, which is the concept of materiality used for this report.

In our current business environment, the longer-term and more comprehensive view of sustainable development is leading to a convergence between social value and enterprise value. Accordingly, assessing the materiality of impact on society for a particular metric can help establish its materiality for enterprise value creation, thereby anticipating potential future developments.

Concerning ‘disclose or explain’, in addition to issues that may not be material for enterprise value creation, other considerations that fall under this mantle might include confidentiality, legal issues or data availability.

Whatever the case, reporting on these ESG metrics demonstrates a commitment to long-term value creation. Companies are encouraged to begin their journey, moving from core disclosures reporting outputs to more sophisticated disclosures, capturing the impacts of their operations on the environment or society, embracing the concept of stakeholder capitalism.

As noted, the metrics have been drawn from existing standards and frameworks, including Global Reporting Initiative (GRI), Sustainability Accounting Standards Board (SASB), Climate Disclosure Standards Board (CDSB), the Natural Capital Protocol, the Value Balancing Alliance, and the Science Based Targets Initiative (SBTi), among others. The source of each of the core and expanded metric is identified in the report along with a rationale for inclusion and additional commentary. For each of the four pillars the relevant UN Sustainable Development Goals are also identified. The appendix to the report includes additional commentary and guidance on reporting.