Common metrics

The result is a collection of core and expanded metrics and disclosures that have been drawn whenever possible from existing standards and disclosures. Selection criteria also included materiality to long-term value creation, universality, extent of actionability, and feasibility of reporting.

Core metrics (24) — These are more established or critically important measures that are already being reported by many organisations, or can be obtained with reasonable effort. They are primarily quantitative metrics focused on activities within the boundaries of the reporting organisation.

Expanded metrics (34) — Less well-established in existing practice, expanded metrics have a wider value chain scope and represent more advanced concepts and measurements for communicating sustainable value creation.

While not intended to replace relevant industry sector, or company-specific indicators, the metrics have been selected for their universality. Companies are encouraged to report on as many metrics as they find material and appropriate based on a “disclose or explain” approach.

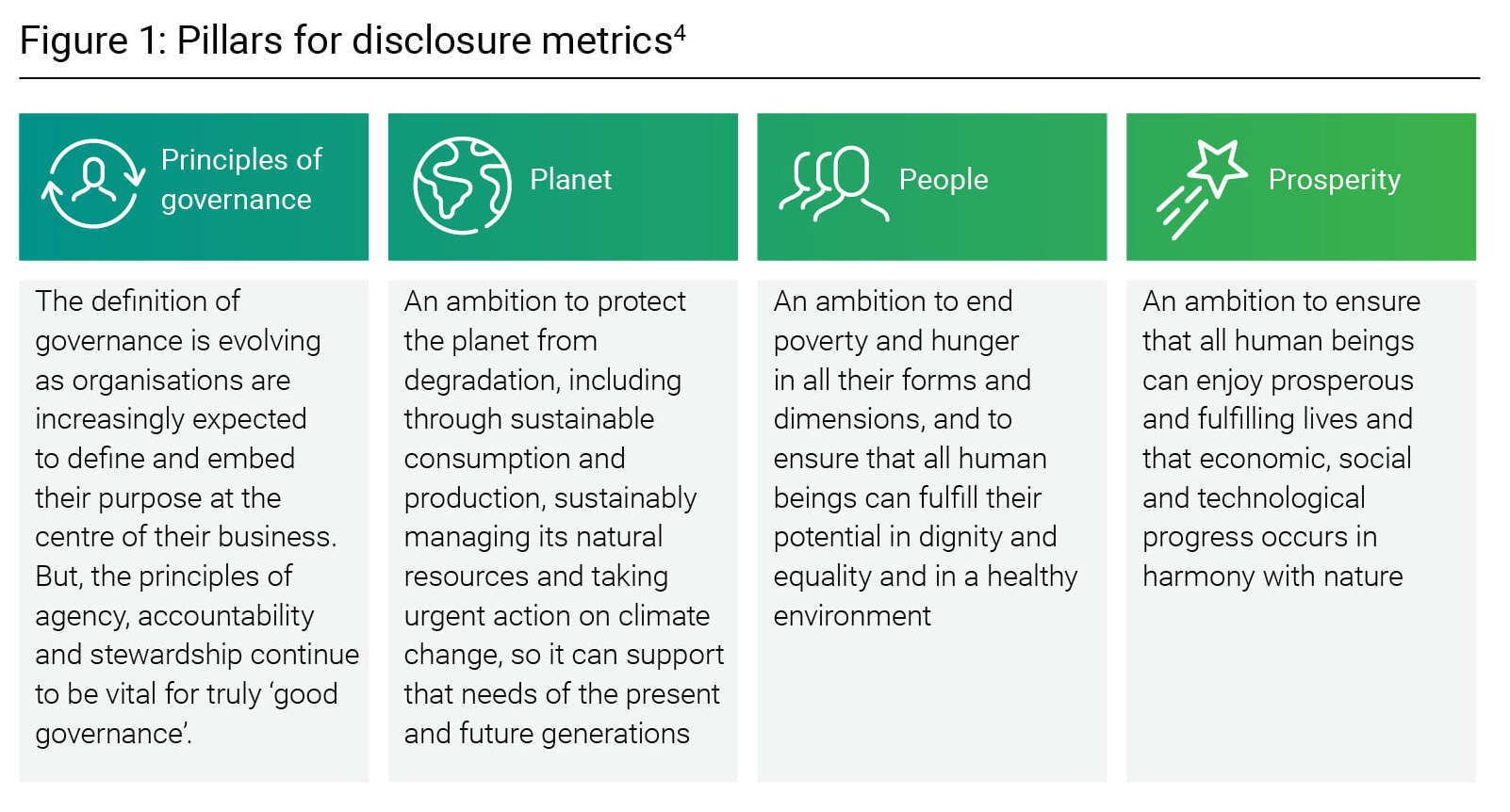

The four pillars

The metrics are organised along the lines of the four pillars of Governance, Planet, People and Prosperity, which are aligned with the UN Sustainable Development Goals (SDGs).3

While each of the pillars is important to the creation of shared sustainable value, they are highly interdependent and should not be taken in isolation.

Core metrics

The core metrics outlined under these four pillars that have also been established thematically are:

1) Principles of Governance

a) Governing purpose i) Setting purpose — Corporate purpose should create value for all stakeholders, including shareholders

b) Quality of governing body i) Governing body composition — Composition of the highest governing by a variety of topics, including ESG competencies

c) Stakeholder engagement i) Material issues affecting stakeholders — A list of topics material to key stakeholders, how they were identified and how stakeholders were engaged

d) Ethical behaviour i) Anti-corruption — In addition to number and nature of incidents, discussion of initiatives, including employee training and stakeholder engagement to combat corruption ii) Protected ethics advice and reporting mechanisms — Internal mechanisms to protect seeking advice and reporting concerns

e) Risk and opportunity oversight i) Integrating risk and opportunity into business process — Opportunities and risks should include material economic, environmental and social issues including climate change and data stewardship

2) Planet

a) Climate change i) Greenhouse gas (GHG) emissions — All relevant gases in CO2 equivalents for GHG Protocol Scope 1 and Scope 2 emissions, and estimates for Scope 3 emissions (upstream and downstream), where appropriate ii) TCFD Implementation — Fully implement Task Force on Climate-related Disclosures (TCFD), or if necessary a timeline within three years for full implementation

b) Nature loss i) Land use and ecological sensitivity — Number and area of sites in, or adjacent to protected areas or key biodiversity areas (KBA)

c) Freshwater availability i) Water consumption and withdrawal in water-stressed areas — report for operations according to WRI Aqueduct water risk atlas tool, including estimates for full upstream and downstream value chain, where appropriate

3) People

a) Dignity and equality i) Diversity and inclusion — Report by the percentage of employees by category ii) Pay equality — The ratio of each relevant priority area of equality by significant locations of operation: women to men, minor to major ethnic groups, etc. iii) Wage level — Ratios of standard entry-level wage compared to a local minimum; the ratio of CEO compensation to the median of employees except CEO iv) Risk for incidents of child forced or compulsory labour — Explanation of operations or suppliers considered to have such risk

b) Health and well-being i) Health and safety — Number and rate of incidents, along with an explanation of how the organization facilitates workers’ access to non-occupational medical and health care services and scope of access provided for employees and workers

c) Skills for the future i) Training provided — Average hours of training per person and average training and development expenditure per full-time employee

4) Prosperity

a) Employment and wealth generation i) Absolute number and rate of employment — Total number of hires and turnover, by age group, gender and other indicators of diversity and region ii) Economic contribution — Direct economic value generated and distributed, including revenues, costs, employee wages and benefits, payments to government, financial assistance received from the government, and community investment iii) Financial investment contribution – including CapEx, share buybacks and dividend payments, along with narratives of strategy for investment and returns of capital to shareholders

b) Innovation of better products and services i) Total R&D expenses — Total costs related to research and development

c) Community and social vitality i) Total tax paid — Total global tax is borne by the company by category of taxes

In addition to the themes highlighted above for the core metrics in each of the four pillar areas, the Planet pillar identified four additional themes for expanded metrics. These included air pollution, water pollution, solid waste and resource availability.