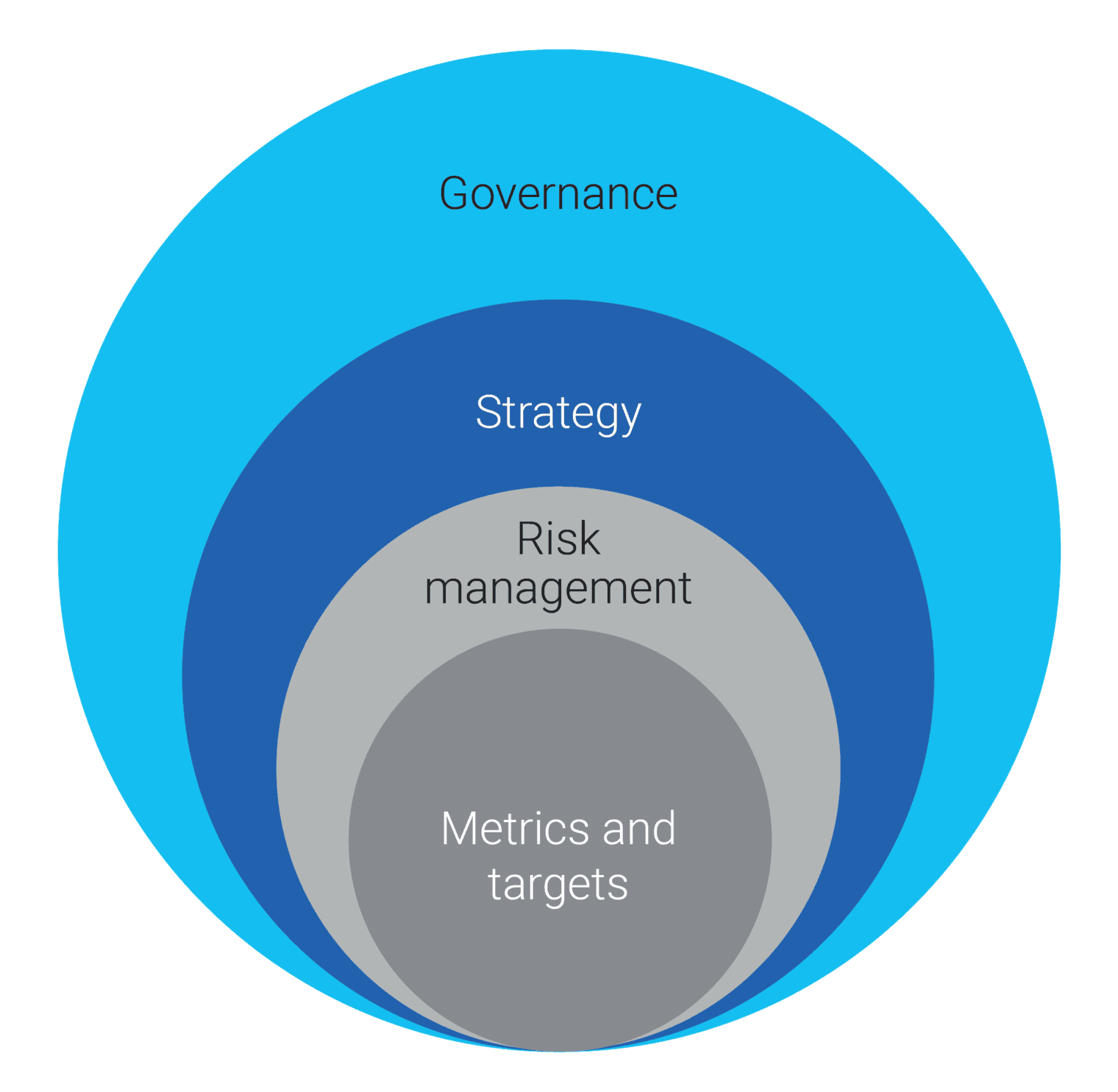

The TCFD recommendations are a framework structured around four core themes of governance, strategy, risk management, and metrics and targets. Key climate-related financial disclosures support these four overarching recommendations. There are recommendations for all organisations, as well as supplemental guidance for specific sectors.

Core themes

Governance — The organisation’s governance around climate-related risks and opportunities

Strategy — The actual and potential impacts of climate-related risks and opportunities on the organisation’s businesses, strategy and financial planning

Risk management — The processes the organisation uses to identify, assess and manage climate-related risks

Metrics and targets — The metrics and targets used to assess and manage relevant climate-related risks and opportunities.

The key to the recommended strategy disclosures, noted above, is to ‘describe the potential impact of different scenarios, including a 2°C scenario, on the organization’s businesses, strategy and financial planning’. Scenario analysis, a well-established method of assessing or analysing the likelihood of a range of possible future states, is discussed extensively in the TCFD recommendations.

Metrics and targets

For metrics and targets, the recommendations specify that reporting entities ‘disclose Scope 1, Scope 2 and, if appropriate, Scope 3 greenhouse gas (GHG) emissions, and the related risks’.

Here is a brief summary of the respective GHG emissions categories:

Scope 1: Direct GHG emissions — These emanate from sources that are owned or controlled by the business; principally the result of the generation of electricity, heat or steam — furnaces, boilers, turbines, etc.; processing of chemicals or materials, e.g. cement, aluminum, waste; transportation of materials, products, employees or waste in company-owned vehicles.

Scope 2: Electricity indirect GHG emissions — This category encompasses emissions from purchased electricity used in a company’s equipment or operations; tracking purchased electricity creates the opportunity to evaluate risks and opportunities of alternative sources of electricity.

Scope 3: Other indirect GHG emissions — These are all indirect emissions (not included in scope 2) that are a consequence of the activities of the business, but that occur from sources not owned or controlled by the business for example, materials suppliers, third-party logistics providers, waste management suppliers, travel suppliers, lessees and lessors, franchisees, retailers, employees, and customers.

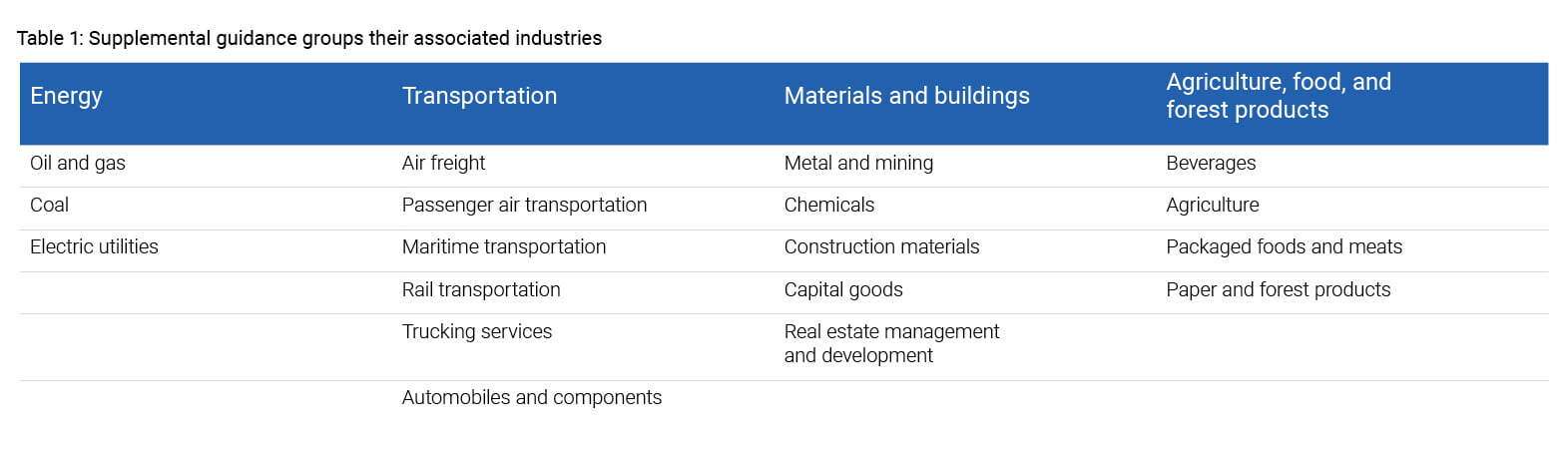

Financial and non-financial sectors

The supplemental guidance the task force created for the finance sector is focused on banks, insurance companies, asset owners and asset managers, including pension plans and foundations. The specific financial sector guidance was generated based on the belief, on the part of the Task Force, that ‘disclosures by the financial sector could foster an early assessment of climate-related risks and opportunities, improve pricing of climate-related risks, and lead to more informed capital allocation decisions’.

The supplemental guidance the task force created for non-financial sectors was based on the 12 industries that account for the largest GHG emissions, energy usage and water usage, broken down into four sectors based on similarities of climate-related risks as highlighted in the table.

Climate-related risks and opportunities

The TCFD categorises the climate-related risks as transition risks — related to the transition to a lower-carbon economy, and physical risks — related to the physical effects of climate change.

The transition risks include policy and litigation risks, technology innovations that may affect competitiveness in addition to market and reputation risks, as customer and community expectations continue to evolve.

The physical risks include acute risks — those that are event-driven, such as extreme weather events like hurricanes, cyclones, flooding or fires; and chronic risks — and those that refer to longer-term shifts in climate patterns, such as higher temperatures, that may contribute to extended heat waves or sea-level rise.

Climate-related opportunities may stem from a variety of sources, including creating efficiencies and innovations, the development of new technologies and products, the formation of new markets, and the financing infrastructure that will meet the needs of a new economy.