The SASB Conceptual Framework is in the process of being revised and has undergone a public comment period. The exposure draft was available for public comment from Aug. 28, 2020, until Dec. 31, 2020.7 It set out proposed changes to the framework and rules of procedure. The following outlined here is based on the 2017 SASB Conceptual Framework that is currently under revision.8

These are industry-specific standards that are used to identify financially material sustainability issues. They intend to provide investors with comparable, non-financial information and metrics across an industry.

The standards include an individual focus across 77 industries. These are arranged by 11 sector categories:

Consumer goods (7 industries)

Extractive and minerals processing (8 industries)

Financial (7 industries)

Food and beverage (8 sectors)

Health care (6 sectors)

Infrastructure (8 sectors)

Renewable resources and alternative energy (6 Industries)

Resource transformation (5 Industries)

Services (7 industries)

Technology and communications (6 industries)

Transportation (9 industries)

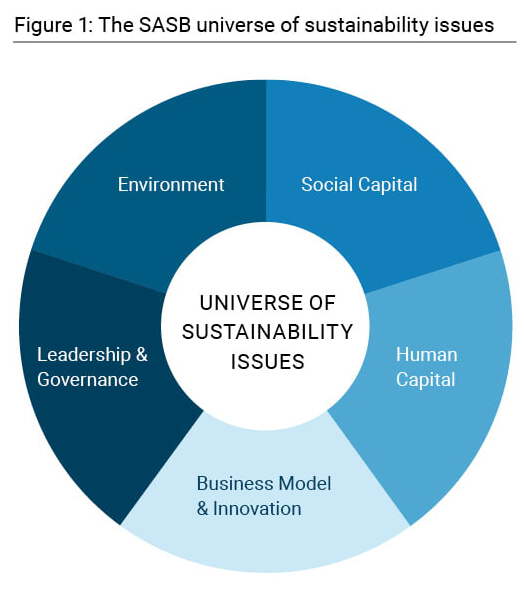

The SASB Materiality Map identifies sustainability issues that are likely to affect the financial condition or operating performance of companies within an industry. There are 26 general categories focusing on broad sustainability issues impacting corporations. These are segmented into five dimensions.

Environment (6 issues)

Social capital (7 issues)

Human capital (3 issues)

Business model and innovation (5 issues)

Leadership and governance (5 issues)