The audience for integrated reporting and the (IR) framework is wide. In addition to the investor, the full range of stakeholders may also be beneficiaries, including customers, employees and suppliers, along with regulators and other parties having an interest in capital markets. Financial professionals working in both management accounting and public accounting are also likely to encounter the (IR) Framework.

As the move towards more comprehensive reporting continues, an increasing number of corporations are beginning to adopt integrated reporting. Companies are also seeking to capitalise on the benefits of integrated thinking that result from this broadening of perspective. Those at the forefront of ESG reporting are also likely to have the (IR) framework on their radar as they consider the benefits of expanding the scope of their reporting. Management accounting professionals with a broad range of accounting, reporting and business skills are well-positioned to provide leadership on this front.

Since the need for assurance is also part of the equation in both sustainability reporting and integrated reporting, public accounting professionals are also increasingly likely to encounter the (IR) framework as the demand for more comprehensive reporting continues.

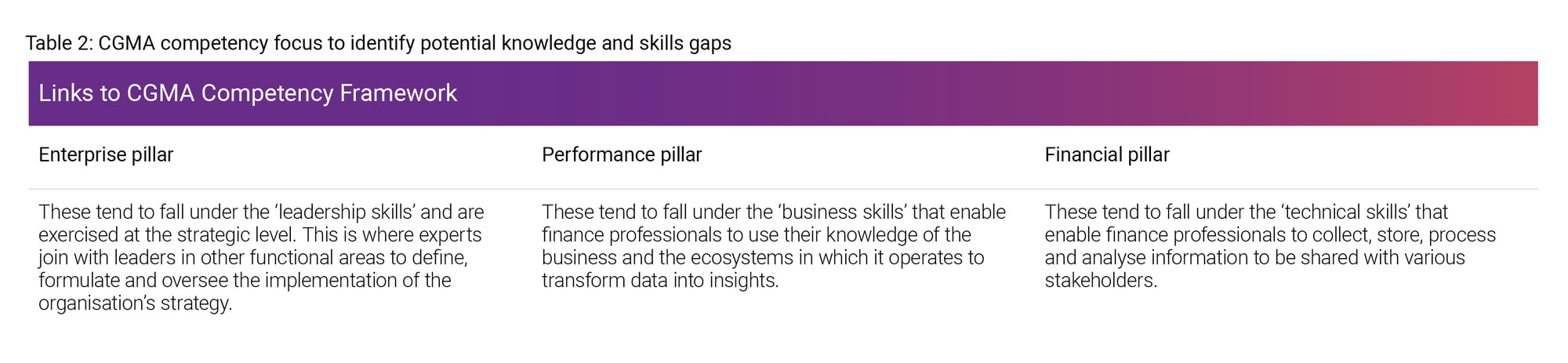

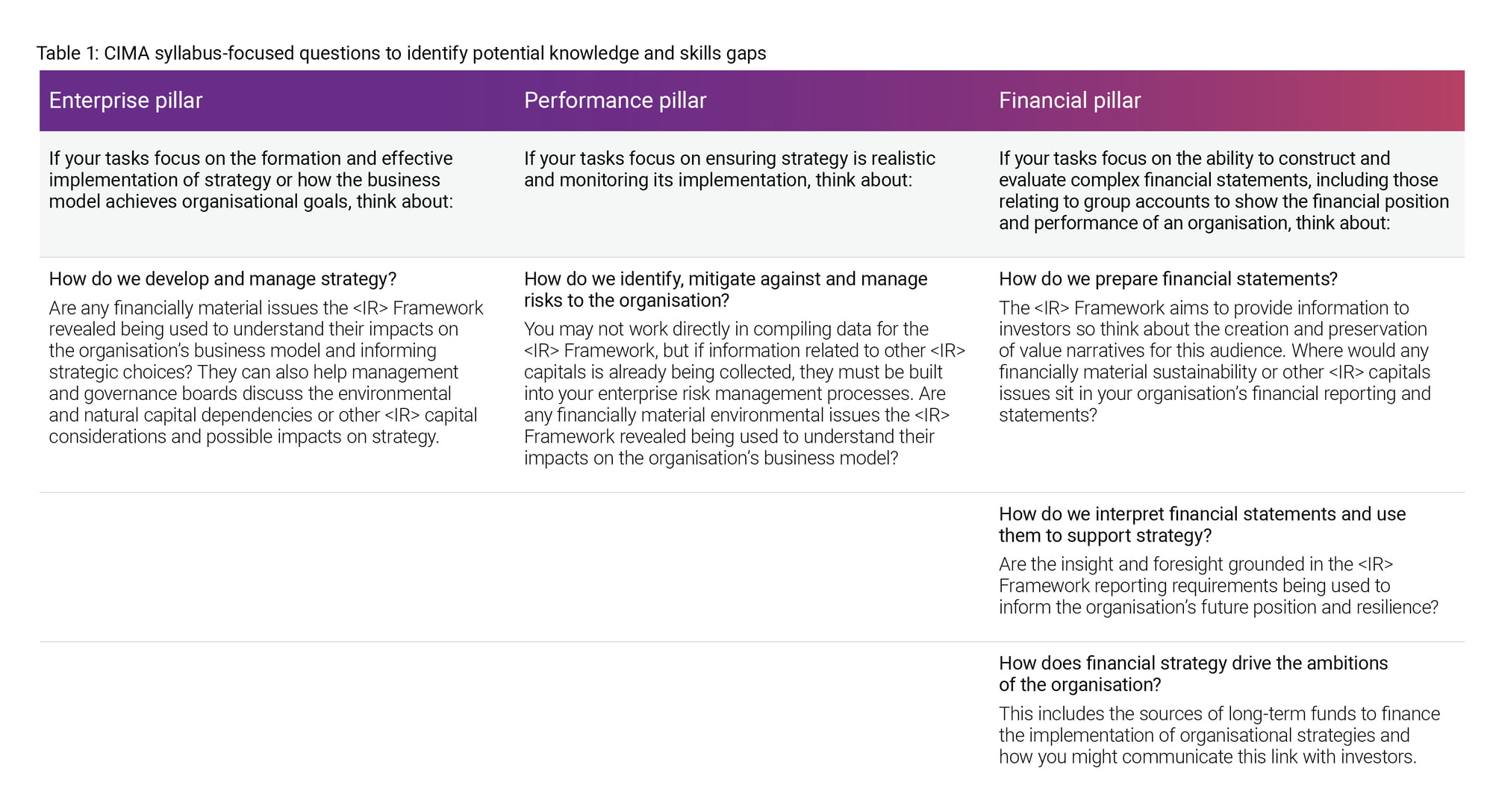

If your organisation is using or contemplating the (IR) framework, the 2019 CIMA® professional qualification syllabus and CGMA competency framework (2019 edition) can help you ask the right questions to identify your potential knowledge and skills gaps.