The (IR) framework provides a principles-based approach to corporate reporting that:

Improves the quality of information available to providers of financial capital

Captures the full range of factors that materially affect an organisation’s ability to create value over time

Enhances accountability and stewardship of the full range of resources that contribute to the value creation process

Supports integrated thinking and decision-making in the organisation that drives the creation of value over the short, medium and long-term6

With this focus on value creation, integrated reporting embraces the notion of integrated thinking, which takes into account the interconnectivity and interdependencies between the various operating and functional units of the business, along with the full range of organisational resources, or “capitals” that contribute to creating value. Integrated thinking encompasses the enterprise’s business model, its strategy and the risks it faces in achieving strategic objectives. It also considers the capacity of the organisation to respond to its external environment and address legitimate key stakeholder needs.

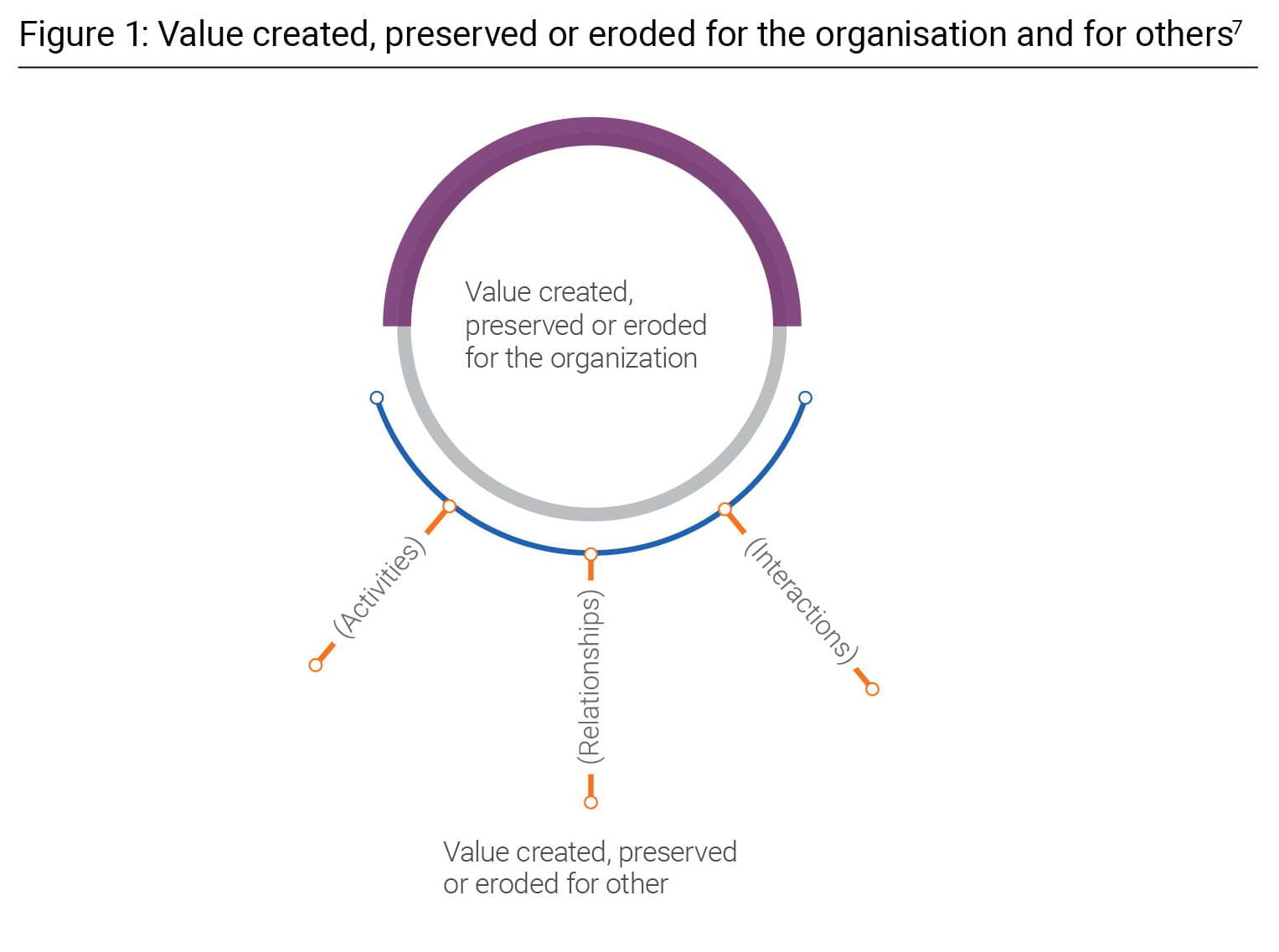

A fundamental concept of Integrated Reporting is that an organisation not only creates value not only for itself but for others (Figure 1). The activities of an organisation affect not only the well-being of customers, suppliers, employees, owners and investors, but also a potentially broad range of other stakeholders and society-at-large. Accordingly, how an organisation carries out these activities also determines any conditions imposed on the organisation’s social license to operate.

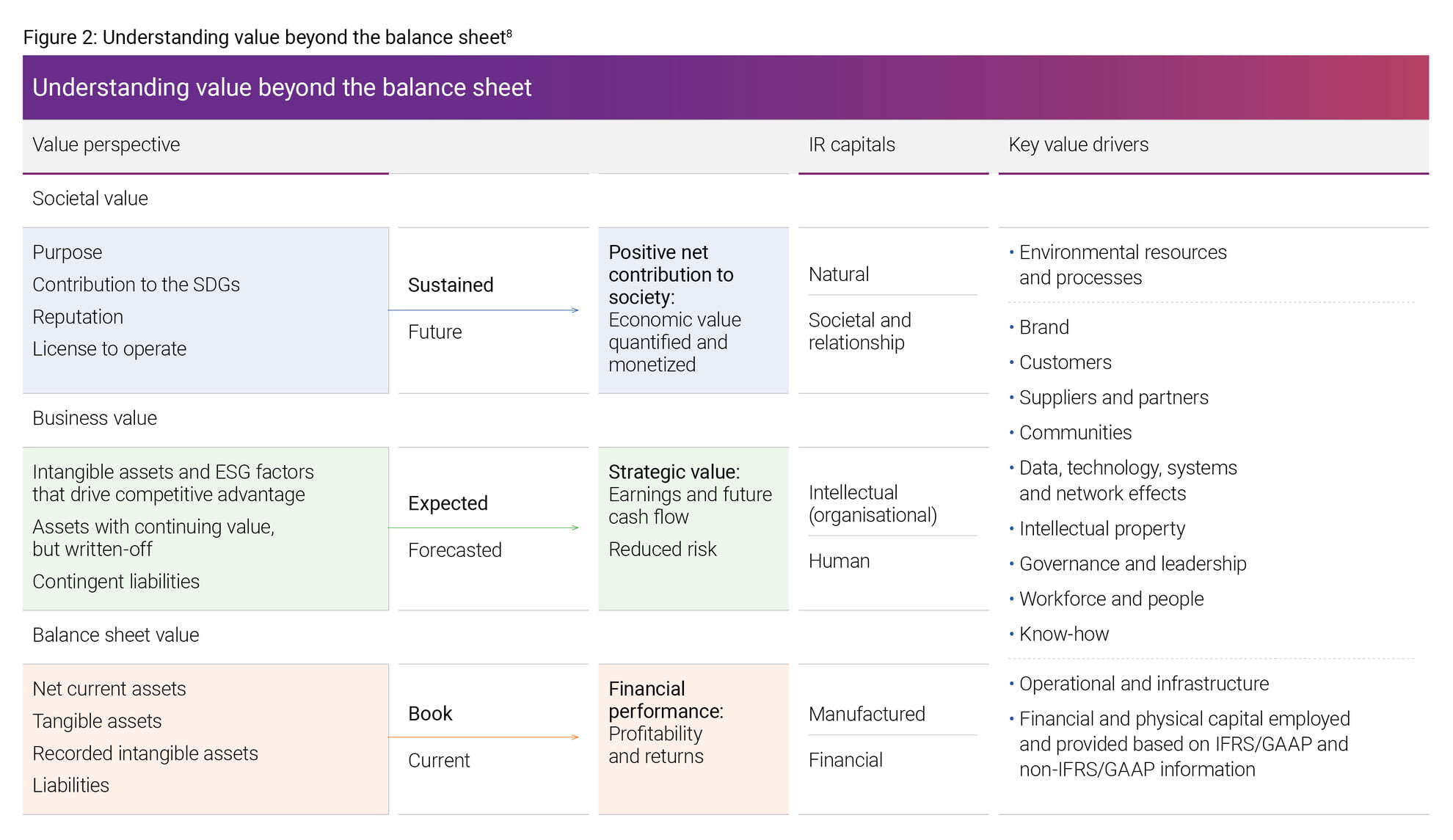

Value beyond the balance sheet

The 2020 report, The CFO and the Finance Role in Value Creation, links key value drivers to the capitals (Figure 2). It captures the essence of the broader view of value creation and reporting through three perspectives:

The balance sheet value perspective Essentially, this captures the ‘book’ value of financial and physical capital based on GAAP accounting standards, along with profitability and returns based on current performance. In addition to providing only this backward-looking view of financial performance, this perspective does not incorporate the strategic value of intangible assets or other assets with value that has been written-off. Nor does it include contingent liabilities that may not meet accounting standards requirements, or ESG factors that may impact competitive advantage or value over a longer-term horizon.

The business value perspective It encompasses these ‘hidden’ components to create a strategic view of expected or forecasted earnings and future cash flows that reflects the organisational intellectual, human and societal and relationship capitals, in addition to manufactured and financial capital. Bringing this broader range of very contextual value drivers into view creates a reduction in the risk profile.

The societal value perspective This moves our thinking beyond this organisationally focused business perspective. Taking a broad approach, this perspective embraces ESG components, including the organisation’s contribution to the U.N. Sustainable Development Goals (SDGs), the net positive and negative impacts of activities on natural capital, and the social and relationship capital considerations that relate to reputation and license to operate. Doing so provides a view of the net contribution of the organisation’s value to society, along with a sense of the ability to sustain that value into the future.