The previous iteration of the GRI Standards provided an option for reporting more limited or more extensive information. The Core reporting option provided the minimum information necessary to understand an organisation, its material impacts and how they are managed. The comprehensive reporting option required additional disclosures on strategy, ethics and integrity, and governance, along with more extensive reporting on impacts

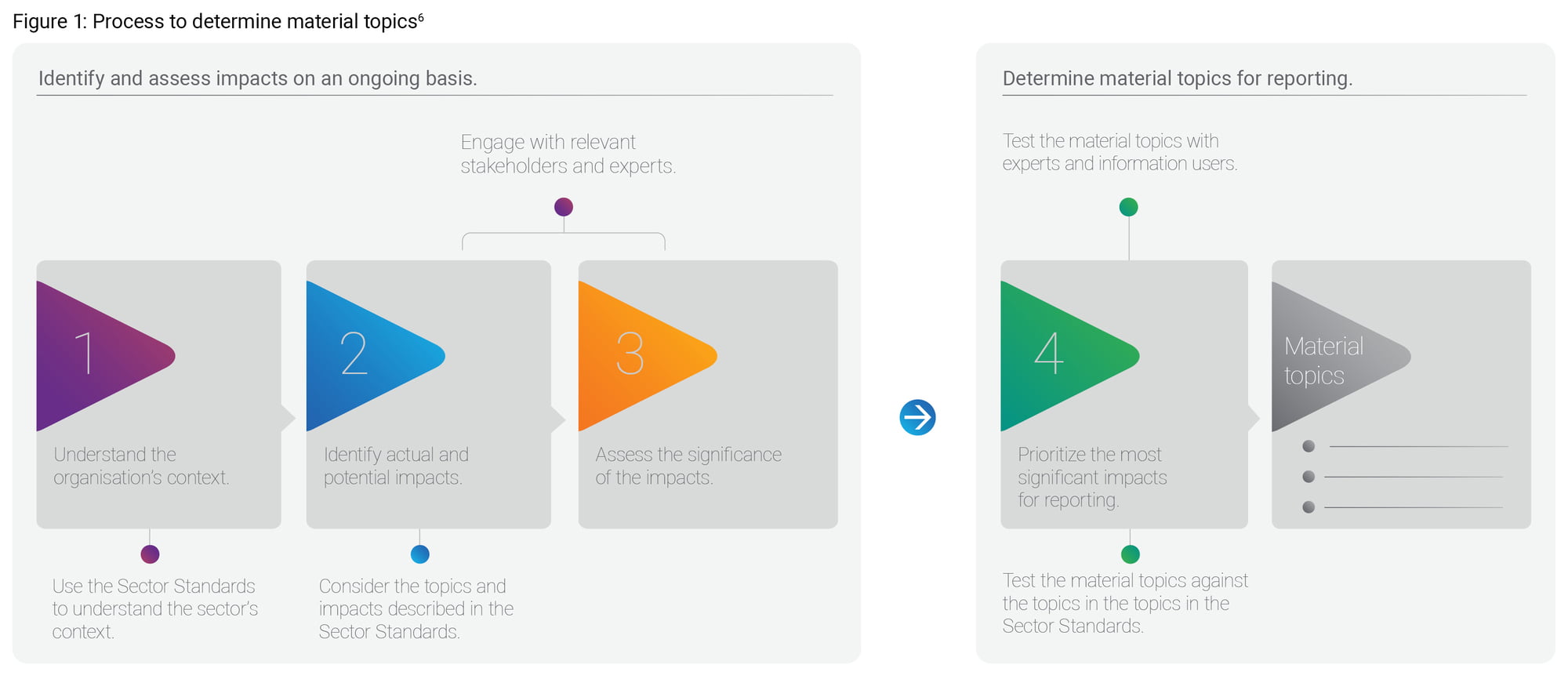

The 2021 version requires companies reporting in accordance with the GRI Standards to determine material topics following a four-step process as summarized in Figure 1.

Material topics are defined as “topics that represent the organization’s most significant impacts on the economy, environment, and people, including impacts on their human rights.”5

These steps involve using the Sector Standards and engaging with relevant stakeholders and experts to first identify actual and potential impacts, then assess their significance. This is followed by testing and prioritising the most significant impacts for reporting.

In addition to reporting on how the organisation manages each material topic, and the extent to which actions taken have been effective, reporting requirements include identifying stakeholders, the organisation’s engagement with them, and the process used for identifying material topics.

The GRI Standards recommend that organisations align sustainability reporting with other reporting, to the extent possible. Also, to enhance the credibility of reporting, the use of internal controls, internal audits, and external assurance are encouraged.

Section 4 of GRI 1: Foundation 2021 includes reporting principles to help organisations ensure the quality and proper presentation of the reported information. These principles are:

Accuracy: Information that is correct and sufficiently detailed to allow an assessment of the organization’s impacts

Balance: Information in an unbiased way and provide a fair representation of the organization’s negative and positive impacts

Clarity: Present information in a way that is accessible and understandable.

Comparability: Select, compile, and report information consistently to enable an analysis of changes in the organization’s impacts over time and an analysis of these impacts relative to those of other organizations.

Completeness: Provide sufficient information to enable an assessment of the organization’s impacts during the reporting period.

Sustainability context: Report information about its impacts in the wider context of sustainable development.

Timeliness: Report information on a regular schedule and make it available in time for information users to make decisions.

Verifiability: Gather, record, compile, and analyze information in such a way that the information can be examined to establish its quality.7