Coincident with the COP 26 meeting in November 2021, the IFRS Foundation announced the formation of the International Sustainability Accounting Standards Board (ISSB) to develop a ‘comprehensive baseline of high-quality sustainability disclosure standards’.16 The intent is for the ISSB to create global standards that are compatible with jurisdiction-specific requirements, such as those contemplated by the EU CSRD or other initiatives in Asia-Oceana, or the Americas. In connection with the formation of the ISSB, the IFRS Foundation also announced its plans to complete the consolidation of the CDSB and the VRF into the new board by June 2022.

In anticipation of that announcement, in support of their commitment to build on existing frameworks and standards, the Trustees had created the Technical Resources Readiness Group of leading organizations which included the TCFD, the Value Reporting Foundation (SASB & IIRC), the CDSB, the World Economic Foundation and the IFRS IASB. Coincident with the announcement of the formation of the ISSB, two prototype standards developed by the TRWG were published. In March 2022, the IFRS Foundation released and published two exposure drafts; Draft IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information, and, Draft IFRS S2 Climate-related Disclosures. Both align with, and build on, the recommendations of the TCFD.17

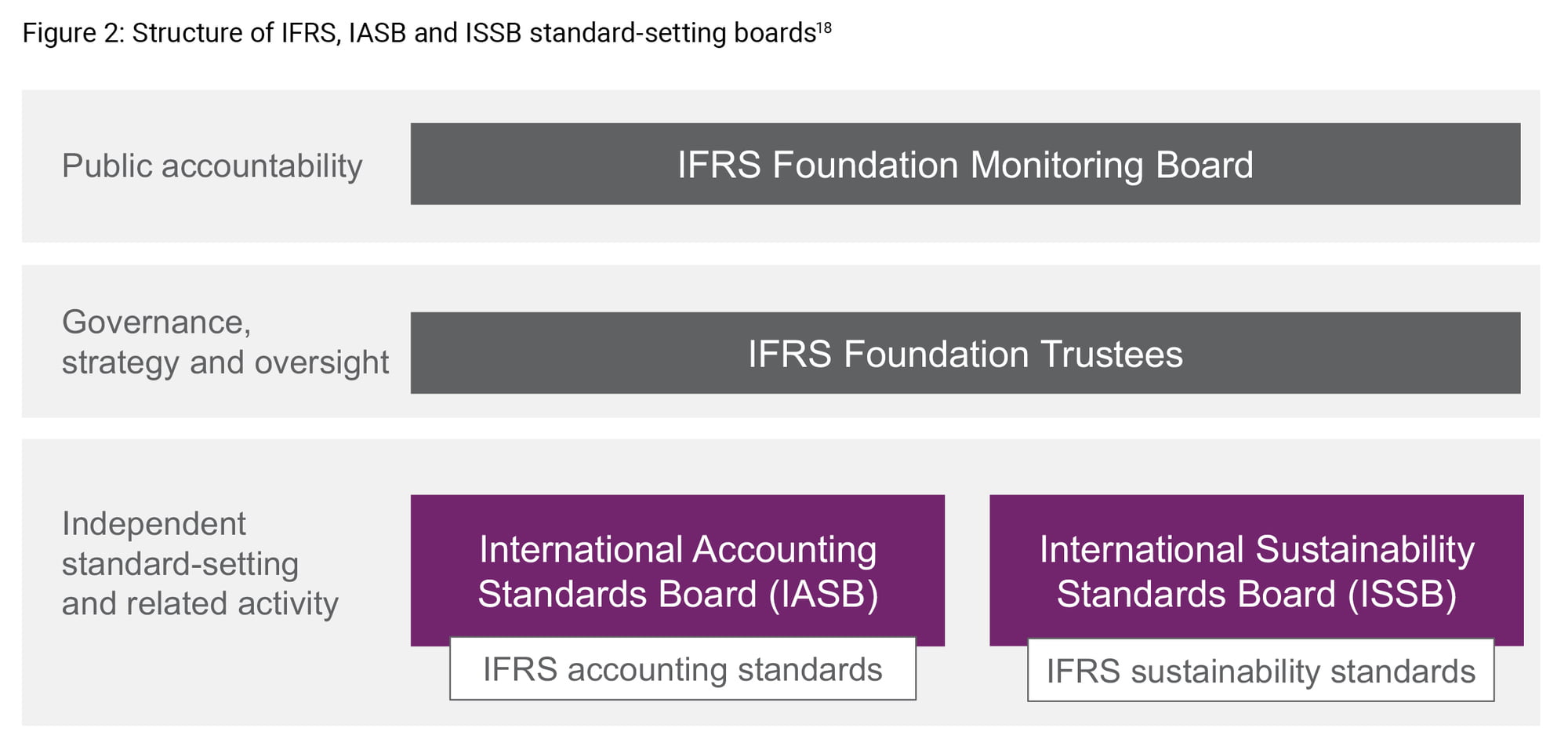

As highlighted in the accompanying diagram, the ISSB will be responsible for IFRS Sustainability Standards and sit alongside the IASB, which is responsible for IFRS Accounting Standards. Governance, strategy and oversight for both will be provided by the IFRS Foundation Trustees. The IFRS Foundation Monitoring Board, which is comprised of public authorities from leading jurisdictions and led by IOSCO, is charged with providing public accountability over both the IASB and the ISSB activities.

Also, as part of the intent to build on existing initiatives, the IFRS announcement addressed plans to leverage the expertise of the CDSB and VRF in the development of reporting standards and also its intention ‘to use the International Integrated Reporting Council to provide advice on establishing connectivity between the work of the IASB and the ISSB via the fundamental concepts and guiding principles of integrated reporting’.19

Concerning SASB, as industry-specific requirements will be established by the ISSB going forward, the SASB Standards will be the primary input source for their development. Since these industry-specific standards will be subject to ISSB due process requirements, the existing SASB Standards will continue to be relevant for some time.

Similarly, the consolidation of the CDSB into the ISSB was consummated in November 2021. As part of the consolidation, the CDSB staff, intellectual property and technical assets were transferred to support the work of the ISSB. As existing CDSB resources will remain relevant and applicable until the publication of ISSB Standards, they will remain accessible via the legacy CDSB website. Notably, in January 2022, the CDSB released a final update to its framework, which included social issues.20 The update also incorporated biodiversity-related considerations into environmental issues, reflecting the recently published CDSB framework Application guidance for biodiversity-related disclosures, launched in November 2021.21