The Statement of Intent underscored the ‘groundswell of demand to understand the connection between sustainability topics and financial risk and opportunity’.5 Critical components of this groundswell include a broadened perspective of the responsibility of business, along with intensified interest for more disclosure about risks and opportunities related to climate change and other ESG components. Asset managers in particular have become increasingly vocal on behalf of their investors about the need for increased disclosure.

The vision the Statement of Intent outlines built on the notion that frameworks and standards that ‘ensure high quality, assurable information, on which the eco-system depends’ create a foundation for reporting that supports more efficient markets and more informed decision-making.6

The goal was to create a ‘similar mindset’ around sustainability information that has evolved for financial information — market acceptance based on reliable, rigorous, transparent and independent standard-setting processes with robust governance. The key to this for sustainability information, as it is for financial information, is the identification of a common set of metrics and disclosure requirements, where possible.

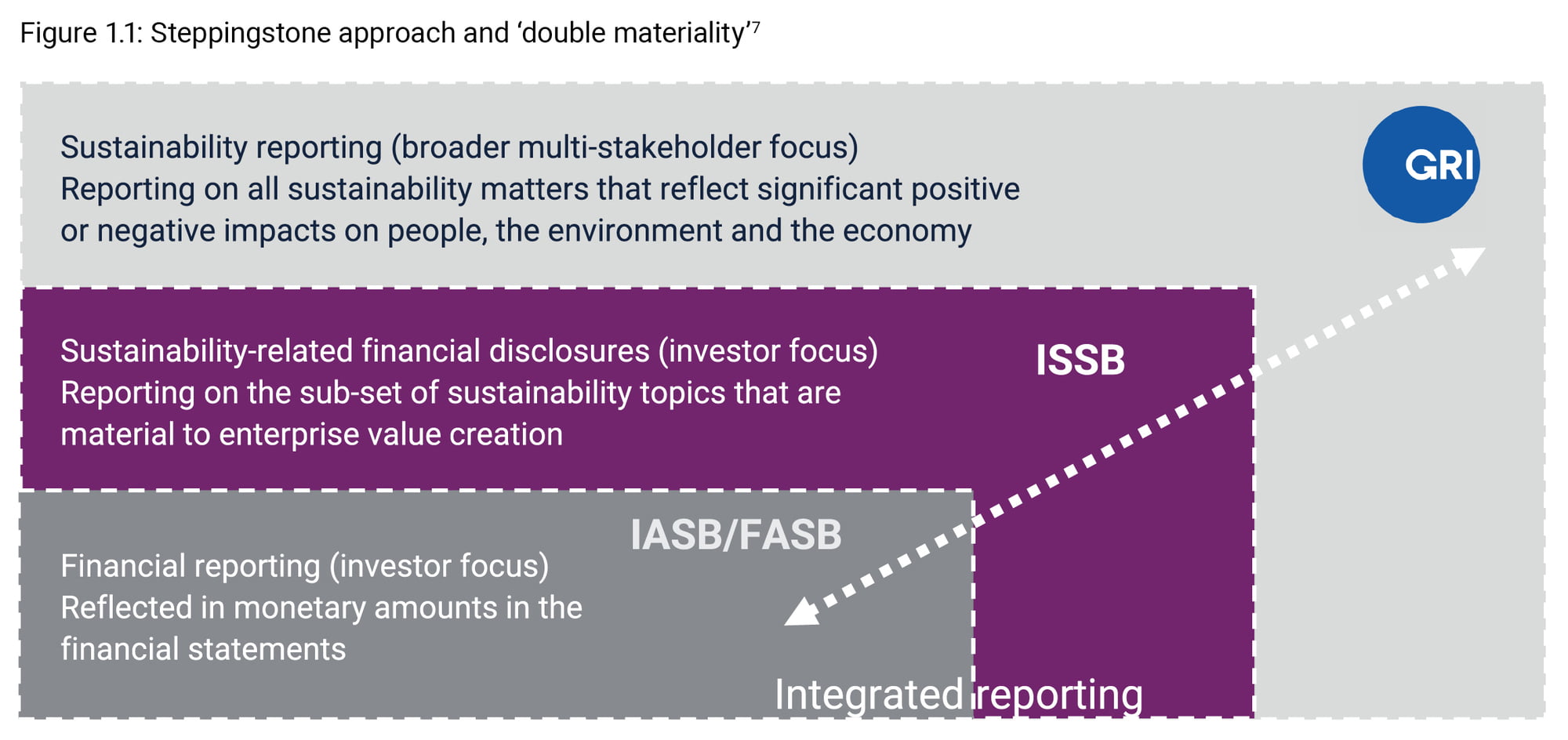

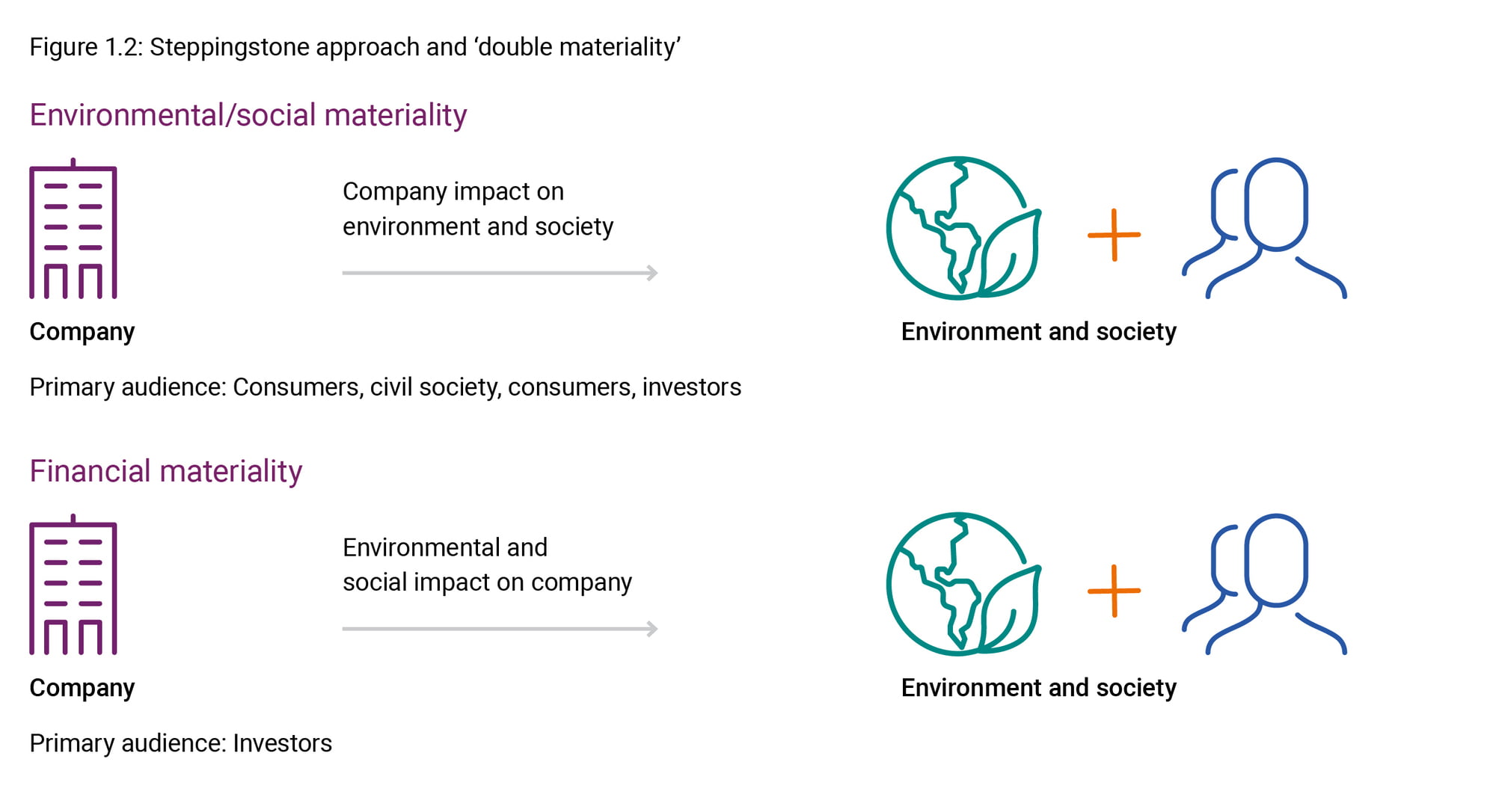

The statement proposed a ‘steppingstone’ or ‘building block’ approach to the standard-setting process that acknowledges the distinct materiality considerations of different stakeholders and corresponding different reporting objectives. This approach, captured by the diagrams in Figures 1.1. and 1.2., which has been updated to reflect the formation of the International Sustainability Standards Board (ISSB), encompasses the ‘double materiality’ concept.

The first building block is based on the standards and frameworks already in existence and in line with current accounting standards. The second building block would be to take an ‘outside-in’ view and incorporate environmental and social issues that are material to the value creation process in an integrated report. The third building block takes an ‘inside-out’ view and expand disclosures to a wider stakeholder group, based on an assessment of the materiality of impacts that the company may have on people, the environment, and the economy. The GRI Framework is the most widely used framework for reporting these impacts.