Nature is far from unlimited. The wild is finite. It needs protecting.

In simple terms, accounting for nature is the process used to measure the impact an organisation has on biodiversity and understand the dependencies for the entity of the natural ecosystem they sit within. This must be considered in the wider context of the planet experiencing dramatic nature loss. Natural capital has traditionally been viewed as a free and unlimited resource, often not reflected in the cost of production, or its impact to the wider stakeholder community rarely accounted for. In many capital allocations and organisational investment decisions investors have ignored nature, and the wider biodiversity issues absent from boardroom decision-making.

Accounting for nature can facilitate the inclusion of environmental resources that are the earth’s natural capital to reflect the true costs of products and services. Directly understanding the material impact of nature on an organisation and the impact of an organisation on nature, not only builds future business resilience, but can also help reverse dramatic nature loss.

The accounting for nature lexicon

In our Environmental Protection Introduction: Putting the E in ESG we summarized some of the aspects of accounting for nature. Included in the summary were concerns about rainforest deforestation and also keystone species such as bees, beavers and hummingbirds, which are critical to the survival of other species in an ecosystem, and especially important to agriculture. We also introduced the concept of ‘movement ecology’, which is the migration of species in response to environmental change.

Upfront, it is important to have a common understanding and definitions of what we mean when using the terms, such as, ‘nature’, ‘biodiversity’ and ‘ecosystem’. The language and terms used are important so that organisations can scope what accounting for nature means for their operations and their wider stakeholder community.

Nature and natural capital

The Oxford English dictionary defines the word ‘nature’ as, ‘all the plants, animals and things that exist in the universe that are not made by people.24 A more common term, in the accounting profession, when thinking about nature, is ‘natural capital’. The IFRS Foundation’s Integrated Reporting <IR> framework defines ‘natural capital’ as,

All renewable and non-renewable environmental resources and processes that provide goods or services that support the past, current or future prosperity of an organization. It includes:

This is broadly in line with the Capitals Coalition definition of ‘natural capital’ and the combined natural resources of ‘plants, animals air, water, soils and minerals.26

With these definitions, at a basic level, accounting for nature, focuses on an organisation’s impact in the four realms of, land, water, freshwater and atmosphere.27 But also the reverse; the impact of nature, or the lack of natural resources, on an organisation.

Ecosystems

The Natural Capital Protocol defines an ecosystem as, ‘A dynamic complex of plants, animals, and microorganisms, and their non-living environment, interacting as a functional unit. Examples include deserts, coral reefs, wetlands, and rainforests.’28 The Canadian Professor of forest ecology, Suzanne Simard, expands on their importance,

Ecosystems are so similar to human societies — they're built on relationships. The stronger those are, the more resilient the system. And since our world's systems are composed of individual organisms, they have the capacity to change. We creatures adapt, our genes evolve, and we can learn from experience. A system is ever-changing because its parts - the trees and fungi and people are constantly responding to one another and to the environment. Our success in coevolution — our success as a productive society — is only as good as the strength of these bonds with other individuals and species. Out of the resulting adaptation and evolution emerge behaviors that help us survive, grow and thrive.29

Biodiversity

A simplified definition of biodiversity, from The Economics of Biodiversity: The Dasgupta Review is, ‘The variety of life in all its forms, and at all levels, including genes, species and ecosystems.' 30 This builds on the United Nations’ Convention on Biological Diversity (CBD) definition of:

The variability among living organisms from all sources, including inter alia, terrestrial, marine and other aquatic ecosystems, and the ecological complexes of which they are part; this includes diversity within species, between species and of ecosystems.31

Biodiversity is critical because it represents the foundation of ecosystems that, through the services they provide, affect human well-being. These services that ecosystems provide include:

provisioning services such as food, water, timber and fiber;

regulating services such as the regulation of climate, floods, disease, wastes and water quality;

cultural services such as recreation, aesthetic enjoyment, and spiritual fulfilment; and

supporting services such as soil formation, photosynthesis and nutrient cycling.

Ecosystems that provide these services include unmanaged ecosystems, such as wildlands and nature preserves, or other ‘protected’ areas; they also include managed systems, ranging from farms, croplands, rangelands to aquaculture sites, as well as urban parks and ecosystems.

Assessing the many dimensions of biodiversity is very complex, and includes attempts to characterize the attributes of ecosystems, their status and their performance, along with measures of ‘ecological capital’, which indicate the amount of resources available for providing services, such as total species and richness, and soil nutrients. These all need to be considered when accounting for nature.

A needed shift in perspective, the three fs: flora fauna and funga:

Often, when thinking about nature, our understanding is biased, by our own senses and simplistic models of the world. Typically for the finance professionals, everything is reduced into a series of abstract, mechanistic components, ending in a financial cost classification. This has been confounded by the Darwinian theory of competition, and the survival of the fittest, that permeates business thinking.

In the world of farming and agriculture, Lake District hill farmer, James Rebanks, noticed,

Our leading agricultural colleges still churn out ‘business-focused’ young farmers, fired up with productive zeal. Students are taught to be at the cutting edge of the new farming, applying science and technology to control nature. They are taught to think about the land like economists. They are taught nothing about tradition, community or ecological limits.32

Shifting perspective in the scientific community includes work in life sciences that is changing our understanding of funga, and it is a prime example of symbiosis. ‘Funga’ is a relatively new collective term for the fungi kingdom, in the same vein as flora is for plants, and fauna is for animals. In 2021, the International Union for the Conservation of Nature (IUCN) called for the recognition of fungi as one of three kingdoms of life critical to protecting and restoring the earth.33 The study of fungi and its symbiotic relationships with plants through mycorrhiza networks challenges our understanding of Darwinian evolution and natural selection.

Understanding nature and becoming nature positive, must promote a symbiotic view of life; one that is the product of cooperation, interaction and mutual dependence.34

There is also a need to move away from thinking that places ’ourselves’ at the centre of everything. Time to consider the richness of the natural world on its own terms and rhythms. This can be hard when many organisations are plugged into data streams, simplified models, and technology running 24 hours a day, that offers instant answers. The data deluge has made it harder for individuals to make decisions. Rather than being more informed, our access to ever-increasing amounts of information is making us less capable of weighing up possible strategic choices, and is disconnecting us from wider natural ecosystems.

Movement ecology is a case in point of slowing down, and observing what is changing in an ecosystem. The study of the movement of wild species, ‘movement ecology’, is providing scientists with early indications, through animal and plant migration, of where climate change impacts are happening.35 Migration patterns are being viewed as a response to environmental change and how an ecosystem functions. This kind of data is also useful to organisations in understanding the next great migration, and how they will need to adapt their business models.

What does nature positive mean?

For organisations, the ultimate aim of accounting for nature must be a journey to become a ‘nature-positive’ entity. This is where an organisation’s activities and impacts upon nature — species and ecosystems — focus on restoration and regeneration rather than facilitating its decline. Where the consideration of complex issues around nature are built into an organisation’s decision-making and business model DNA. Being Nature positive is a DNSH philosophy — ‘Do No Significant Harm.’

The Taskforce on Nature-related Financial Disclosure (TNFD) define the term, ‘nature positive’ as, ‘A high-level goal and concept describing a future state of nature (e.g., biodiversity, ecosystem services and natural capital) which is greater than the current state.’36 Guidance from the Science Based Targets Network adds time scales to what it means to be nature positive, ‘a nature-positive world requires no net loss of nature from 2020, a net positive state of nature by 2030, and full recovery of nature by 2050’.37

For individuals and organisations looking to pursue being nature positive, a first step is to explore the Convention on Biological Diversity’s (CBD) The Kunming-Montreal Global Biodiversity Framework38 Its vision, goals and targets can help provide the focus for an organisation’s the journey to becoming nature positive.

UN Biodiversity Conference (COP15) — December 2022

Delayed from meeting in 2020, due to the COVID-19 pandemic, the 15th conference of the parties (COP) under the Convention on Biological Diversity (CBD) met in December 2022. 195 countries and the European Union came together in Montreal, Canada, to agree a new set of global goals to protect and restore nature by 2050. Billed as the biggest biodiversity conference in a decade, the Kunming-Montreal Global Biodiversity Framework (GBF), is being heralded as the nature equivalent to the 20215 Paris agreement on Climate.

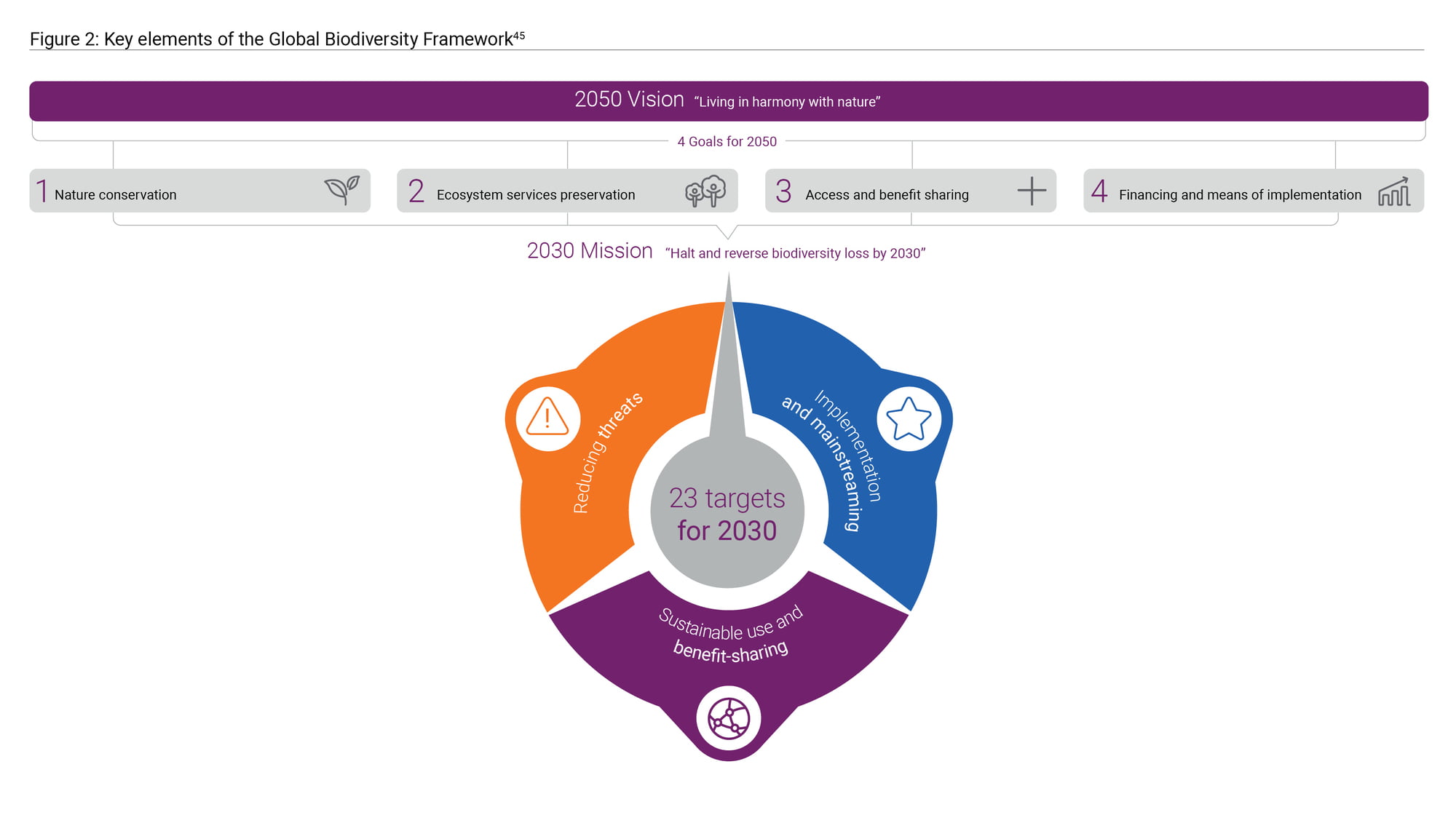

The Kunming-Montreal Global Biodiversity Framework has a vision for 2050 and four supporting goals. Its vision,

By 2050, biodiversity is valued, conserved, restored and wisely used, maintaining ecosystem services, sustaining a healthy planet and delivering benefits essential for all people.39

The vision for 2050 is supported by four long-term goals. These are,

Nature conservation The integrity, connectivity and resilience of all ecosystems are maintained, enhanced, or restored, substantially increasing the area of natural ecosystems by 2050; Human-induced extinction of known threatened species is halted, and, by 2050, the extinction rate and risk of all species are reduced tenfold and the abundance of native wild species is increased to healthy and resilient levels; The genetic diversity within populations of wild and domesticated species, is maintained, safeguarding their adaptive potential.40

Ecosystem services preservationBiodiversity is sustainably used and managed and nature’s contributions to people, including ecosystem functions and services, are valued, maintained and enhanced, with those currently in decline being restored, supporting the achievement of sustainable development for the benefit of present and future generations by 2050.41

Access and benefit sharingThe monetary and non-monetary benefits from the use of genetic resources, and digital sequence information on genetic resources, and of traditional knowledge associated with genetic resources, as applicable, are shared fairly and equitably, including, as appropriate, with indigenous peoples and local communities, and substantially increased by 2050, while ensuring traditional knowledge associated with genetic resources is appropriately protected, thereby contributing to the conservation and sustainable use of biodiversity, in accordance with internationally agreed access and benefit-sharing instruments.42

Financing and means of implementationAdequate means of implementation — including financial resources, capacity-building, technical and scientific cooperation, and access to and transfer of technology — to fully implement the Kunming-Montreal global biodiversity framework are secured and equitably accessible to all Parties. This is especially true in developing countries, in particular the least developed countries and small island developing states. That includes countries with economies in transition, progressively closing the biodiversity finance gap of 700 billion dollars per year, and aligning financial flows with the Kunming-Montreal Global Biodiversity Framework and the 2050 Vision for Biodiversity.43

The GBF then introduces 23 action-oriented targets. These have been designed for and urgent response over the next decade, with a 2030 mission:

To take urgent action to halt and reverse biodiversity loss to put nature on a path to recovery for the benefit of people and the planet by conserving and sustainably using biodiversity, and ensuring the fair and equitable sharing of benefits from the use of genetic resources, while providing the necessary means of implementation.44

The GBF then introduces 23 action-oriented targets. These have been designed for and urgent response over the next decade, with a 2030 mission.

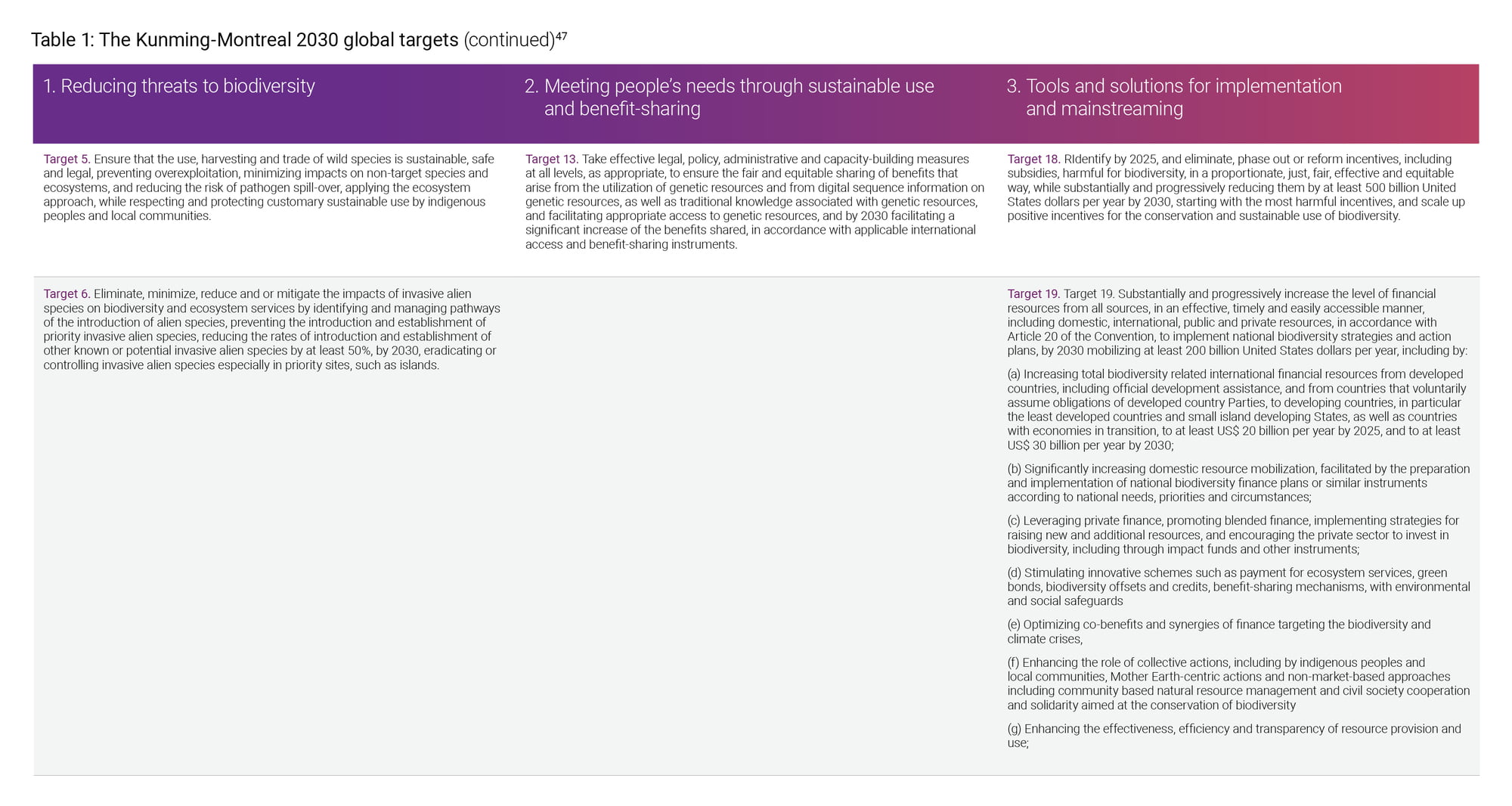

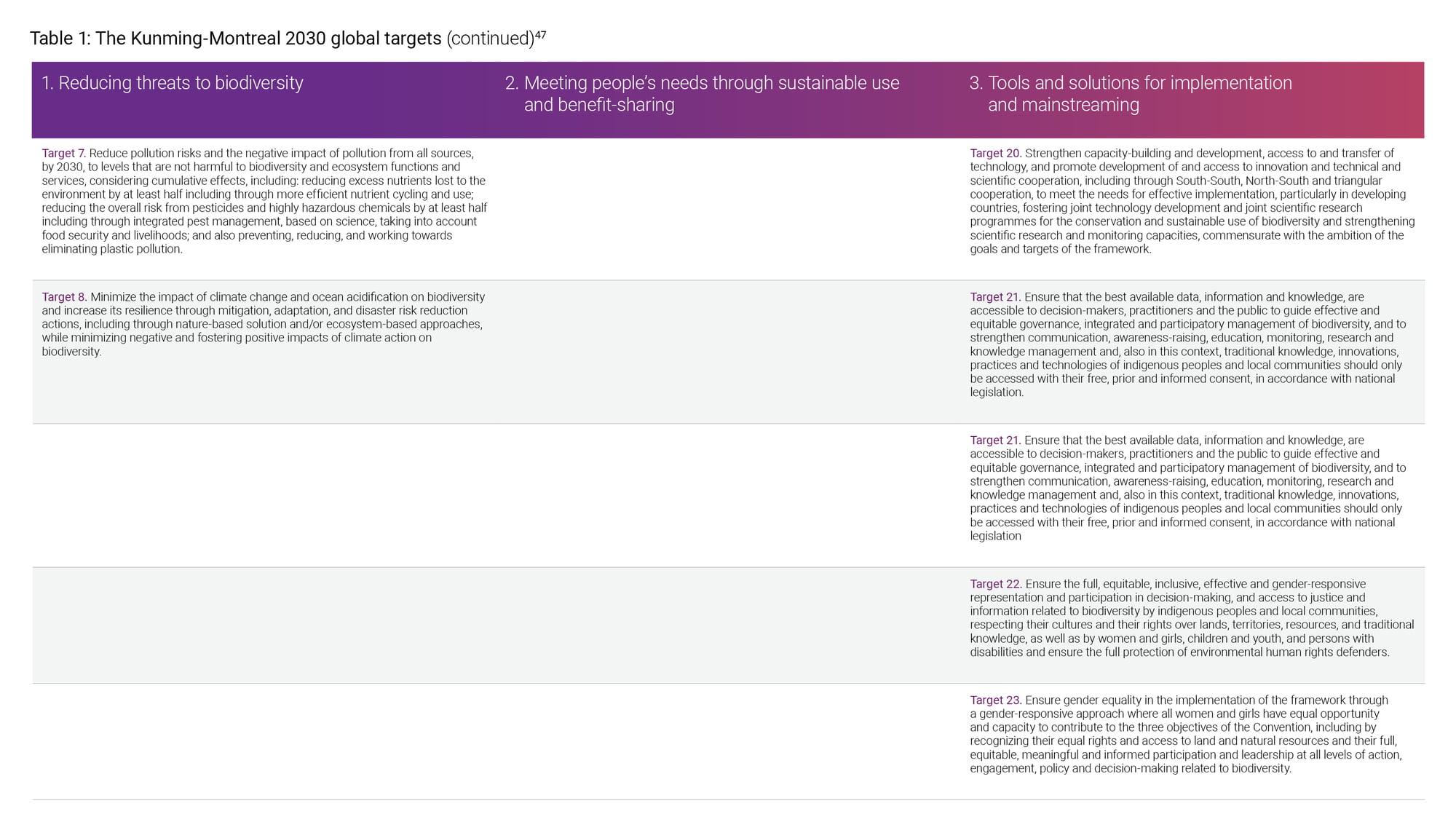

The 23 action-oriented targets are divided into three categories

Reducing threats to biodiversity (8 targets)

Meeting people’s needs through sustainable use and benefit-sharing (5 targets)

Tools and solutions for implementation and mainstreaming (10 targets).

Reducing threats to biodiversity targets relate primarily to land and sea use and conservation efforts, along with restoration of degraded freshwater, marine and terrestrial ecosystems.

Targets under the category of meeting people’s needs encompass sustainable management and equitable use of agriculture, aquaculture and forestry resources, along with access to, and benefits of ‘green and blue spaces’, especially in urban and other densely populated areas.

Tools and resources for implementation and mainstreaming relate to socio-political and economic activities, along with the values, incentives and behaviours necessary to ensure either positive or neutral biodiversity.

To build their accounting for nature literacy, the finance professional and their organisations should start by understanding the following draft targets and the implications to business.

Target 14 — Ensure the integration of biodiversity into policies, regulations, and development processes.

This target involves the assessment of impacts ‘at all levels of government and across all sectors of the economy’ to ensure alignment with biodiversity values.

Target 15 — Take legal, administrative or policy measures to encourage and enable business, and in particular to ensure that large and transnational companies and financial institutions: (a) Regularly monitor, assess, and transparently disclose their risks, and (b) Provide information needed to consumers to promote sustainable consumption patterns. (c) Report on compliance with access and benefit-sharing regulations and measures.

Mandatory nature disclosure is due to be implemented within the European Union in 2023 with the introduction of the with the Corporate Sustainability Reporting Directive (CSRD).

Target 16 — Ensure that people are encouraged and enabled to make sustainable consumption choices.46

For people and consumers to be enabled to make sustainable consumption choices, this will require organisations to disclose more of their products’ impacts on nature. A greater understanding of products’ materiality on nature and stakeholders will help here. For more details see ‘materiality and externalities in accounting for nature’ section.

The Sustainable Development Goals and nature (SDGs)

In September 2015, the United Nations established its 17 Sustainable Development Goals. The goals recognise,

that ending poverty must go hand-in-hand with strategies that build economic growth and address a range of social needs, including education, health, equality and job opportunities, while tackling climate change and working to preserve our ocean and forests.48

At a simple level there are two goals that relate specifically to nature. These are,

14 Life below water — Conserve and sustainably use the oceans, seas and marine resources for sustainable development.

15 Life on land — Protect, restore and promote sustainable use of terrestrial ecosystems, sustainably manage forests, combat desertification, and halt and reverse land degradation and halt biodiversity loss.

However, to only consider SDG 14 and 15 encourages lazy thinking, and not what the goals were defined to promote. Nature is a topic that cuts across, and is interconnected, with many of the other goals. This interconnectedness must be reflected when accounting for nature. For example, goals, 6 clean water and sanitation, 11 sustainable cities and communities, 12 Responsible consumption and production, and 13 climate action, all directly impact and contribute to increasing nature and biodiversity loss if not kept in check. Then if nature and biodiversity loss is not reversed there will be an increasing negative impact on the goals; 1 no poverty, 2 zero hunger, and, 3 good health and well-being.

1 No poverty — End poverty in all its forms everywhere.

2 Zero hunger — End hunger, achieve food security and improved nutrition and promote sustainable agriculture.

3 Good health and well-being — Ensure healthy lives and promote well-being for all, at all ages.

6 Clean water and sanitation — Ensure availability and sustainable management of water and sanitation for all.

11 Sustainable cities and communities — Make cities and human settlements inclusive, safe, resilient and sustainable.

12 Responsible consumption and production — Ensure sustainable consumption and production patterns.

13 Climate Action — Take action to combat climate change and its impacts

Here the creation of an organisational purpose map is helpful to understand the impact of nature. It also highlights the relevance of each of the goals and the relationship between an organisation and its wider ecosystem. Start by categorising the goals by those,

That are part of the core organisation activity.

That are important to the organisation.

Over which the organisation has influence.

Fundamentally, without nature and biodiversity stability any organisational efforts to achieve goal 8, decent working and economic growth would be impossible. Download our SDGs Brief 50

Materiality and externalities in accounting for nature

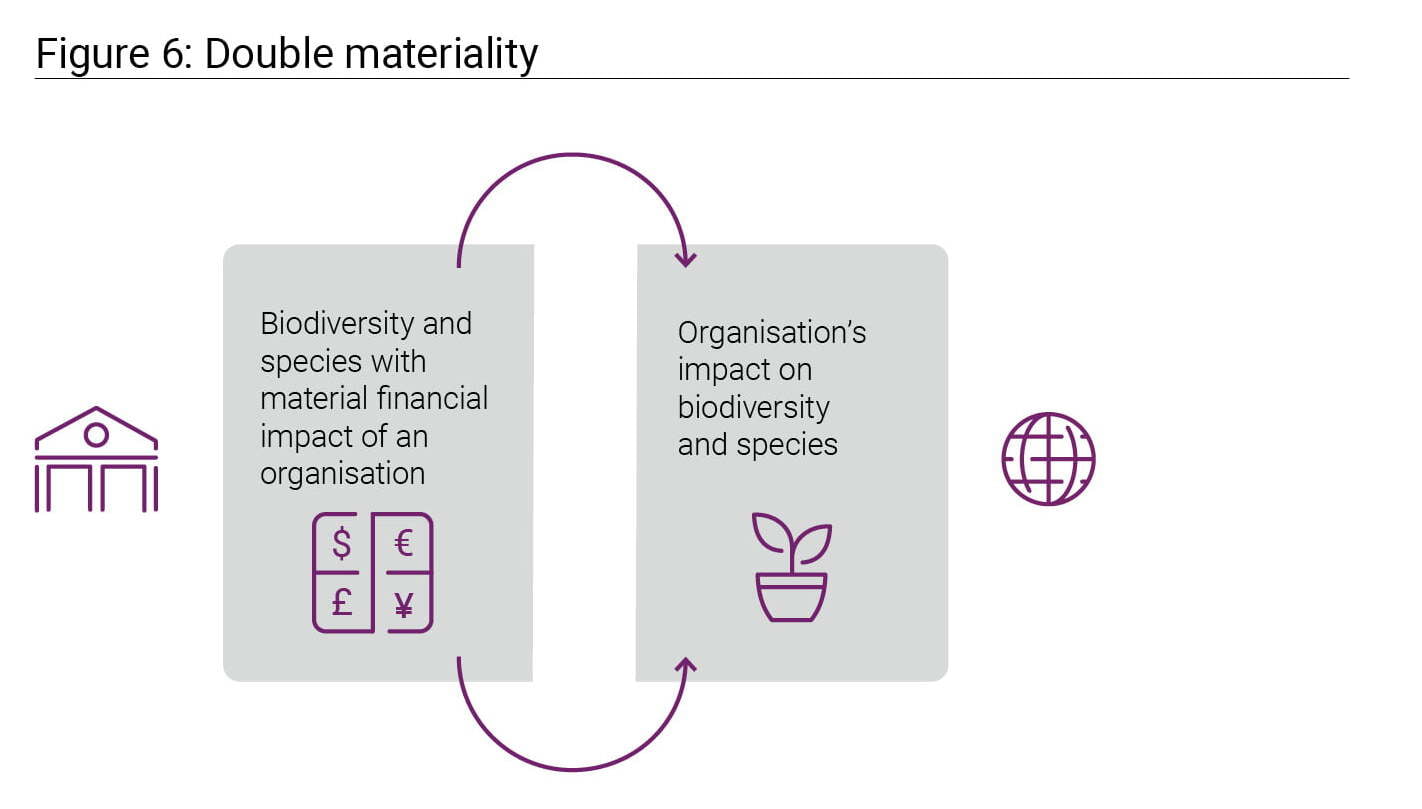

The Integrated Reporting <IR> framework defines materiality as, ‘A matter is material if it could substantively affect the organization’s ability to create value in the short, medium or long term.’51 However, materiality is a dynamic concept as issues are not always easily identified, their relevant stakeholders defined, or their long-term significance fully understood. It is also an area that is very subjective.

Adding to the complexity of accounting for nature is using different terminology in defining the same or similar activity around materiality. Terms include, ‘financial materiality’, ‘impact materiality’, ‘nested materiality’ and ‘dynamic materiality’.52

The EU Non-Financial Reporting Directive (NFRD) and the Global Reporting Imitative (GRI) standards use the term, ‘double materiality’. This is where organisations not only disclose how sustainability (in this case nature) issues affect them, but also how organisations affect the environment and society — an organisation’s view of ‘outside-in risks’ and ‘inside-out risks’.53 The double materiality principle leads to organisations disclosing information on their nature mitigation and adaptation plans to become nature positive.

Externalities are the ‘benefits or costs arising from an activity, which does not accrue to the entity of person carrying on the activity.’54 This is an important concept when accounting for nature, as for many organisations, the costs of using natural resources and potential negative impacts, such as air pollution or deforestation, are often not reflected in market pricing. Accounting for nature involves recognizing the true cost environmental and social resources when making organisational investment and pricing decisions.55

Keystone species and extinction accounting

These areas are growing in importance for many industries dependent on agriculture. A keystone species is an organism that helps define an entire ecosystem, such as a bee, which is a pollinator for fruits, nuts and other crops. For a forest situation, the mycorrhiza fungi network for trees could be considered the keystone species. Since any crops are often grown in concentrated geographical locations, ‘a monoculture’, the surrounding communities are especially vulnerable to the possible decline of the keystone species. Some facts on monocultures from the author and journalist, Dan Saladino,

… the source of much of the world's food seeds — is mostly in the control of just four corporations; half of all the world's cheeses are produced with bacteria or enzymes manufactured by a single company; one in four beers drunk around the world is the product of one brewer; from the USA to China, most global pork production is based around the genetics of a single breed of pig, and, perhaps most famously, although there are more than 1,500 different varieties of banana, global trade is dominated by just one, the Cavendish, a cloned fruit grown in monocultures so vast their scale can only be comprehended from the view of an airplane or by satellite.56

If an organisation’s business model is dependent on a ‘monoculture’ natural resource now is the time to consider the implications as part of the Enterprise Risk Management (ERM) processes.

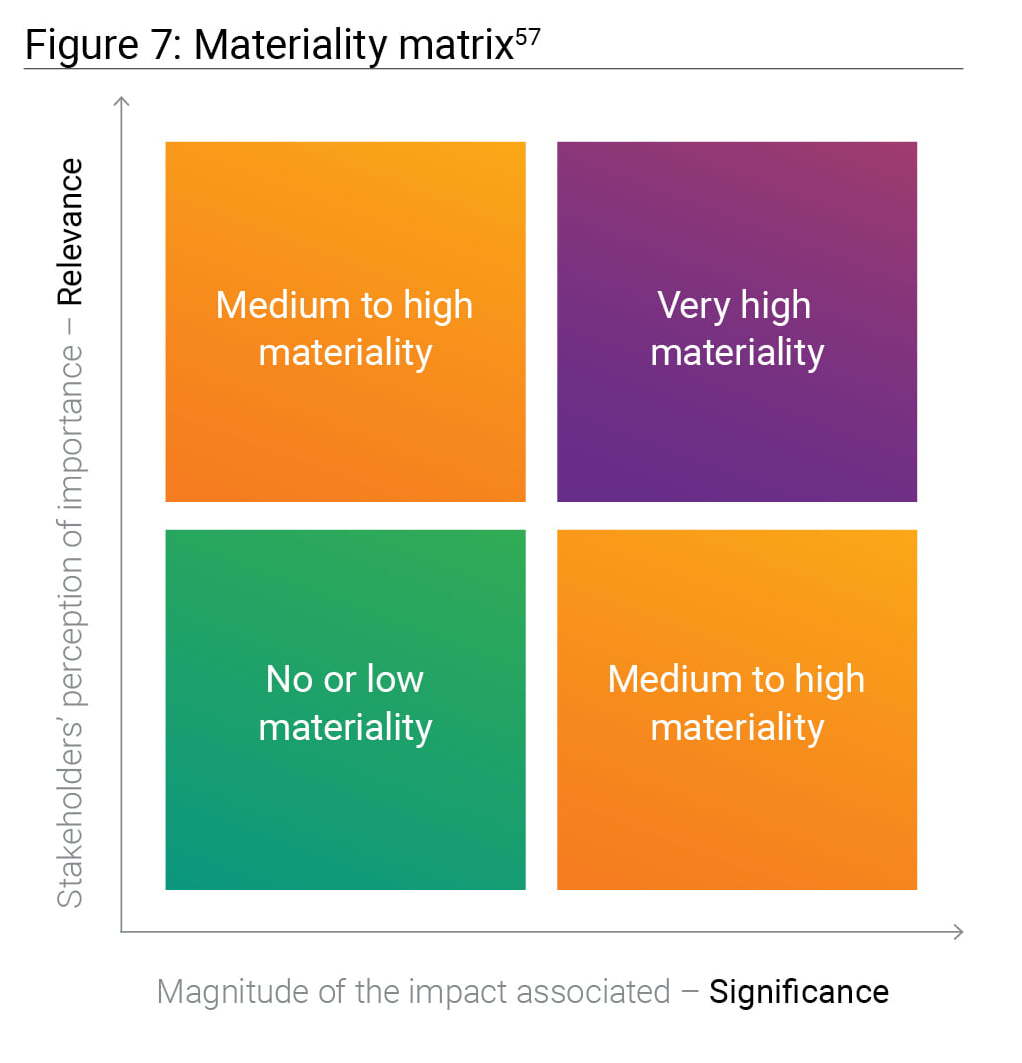

Stakeholders and a materiality matrix

Finally, it is important to be able to demonstrate to stakeholders how an organisation’s strategy contributes to nature and society. One way of doing this is to identify and quantify impact pathways (Inputs — Activities — Outputs — Outcomes — Impacts) through the strategy and link them into the corresponding stakeholder groups.

With the level of complexity in accounting for nature and the number of material stakeholders, organisations must think about what and how to report issues in a transparent, and nature-positive way. Building a stakeholder materiality matrix can help provide clarity.

The scope of accounting for nature: standards, frameworks and future regulation

A finance professional is likely to encounter one or many of the general sustainability frameworks and standards, and those that specifically target nature. It is currently a fragmented landscape, with slightly different terms, inconsistent language and various measures between the methodologies. The definition of what is material (see above) demonstrates the possible confusions. Adding to the confusion is whether adoption is voluntary or mandatory, and that some organisations work with combinations of standards and frameworks at the same time. Finally, the approaches to reporting also differ. They range from annual reports, integrated reports, sections on an organisation’s website aimed at a specific audience, or a stand-alone sustainability report.

Fortunately, there are several initiatives underway to address this fragmented sustainability accounting and reporting landscape, and build a coherent global approach to corporate reporting, that encompasses both financial and non-financial reporting.

The adoption of the goals and targets from The Kunming-Montreal Global Biodiversity Framework will play a part in helping provide focus across nature standards and frameworks.

Regulators and governments are progressively focused on the topic of nature and biodiversity loss, so increased legislation and reporting will affect organisations over the next five years. Again, the adaptation of the global biodiversity framework will focus governments to develop national goals, targets, and measures to reverse biodiversity loss. Once national country plans have been developed, their implementation will be placed on organisations to contribute towards.

Standards and frameworks

The Taskforce on Nature-related Financial Disclosure (TNFD) draft framework

The Taskforce on Nature-related Financial Disclosure (TNFD) was established in 2021 with the mission,

To develop and deliver a risk management and disclosure framework for organisations to report and act on evolving nature-related risks, with the ultimate aim of supporting a shift in global financial flows away from nature-negative outcomes and towards nature-positive outcomes.58

The TNFD plans to develop a framework for release in November 2023. It will allow organisations to build, ‘nature-related risks and opportunities into their strategic planning, risk management and asset allocation decisions.’ Based on seven principles (market usability, science-based, nature-related risks, purpose-driven, integrated & adaptive, climate-nature nexus and globally inclusive) the second beta version of the TNFD framework was released in June 2022.59

The framework uses a nature-related risk and opportunity assessment approach called ‘LEAP’. LEAP is an approach involving four core phases of analytic activity. These are,

Locate your interface with nature;

Evaluate your dependencies and impacts;

Assess your risks and opportunities; and

Prepare to respond to nature-related risks and opportunities, and report to investors.60

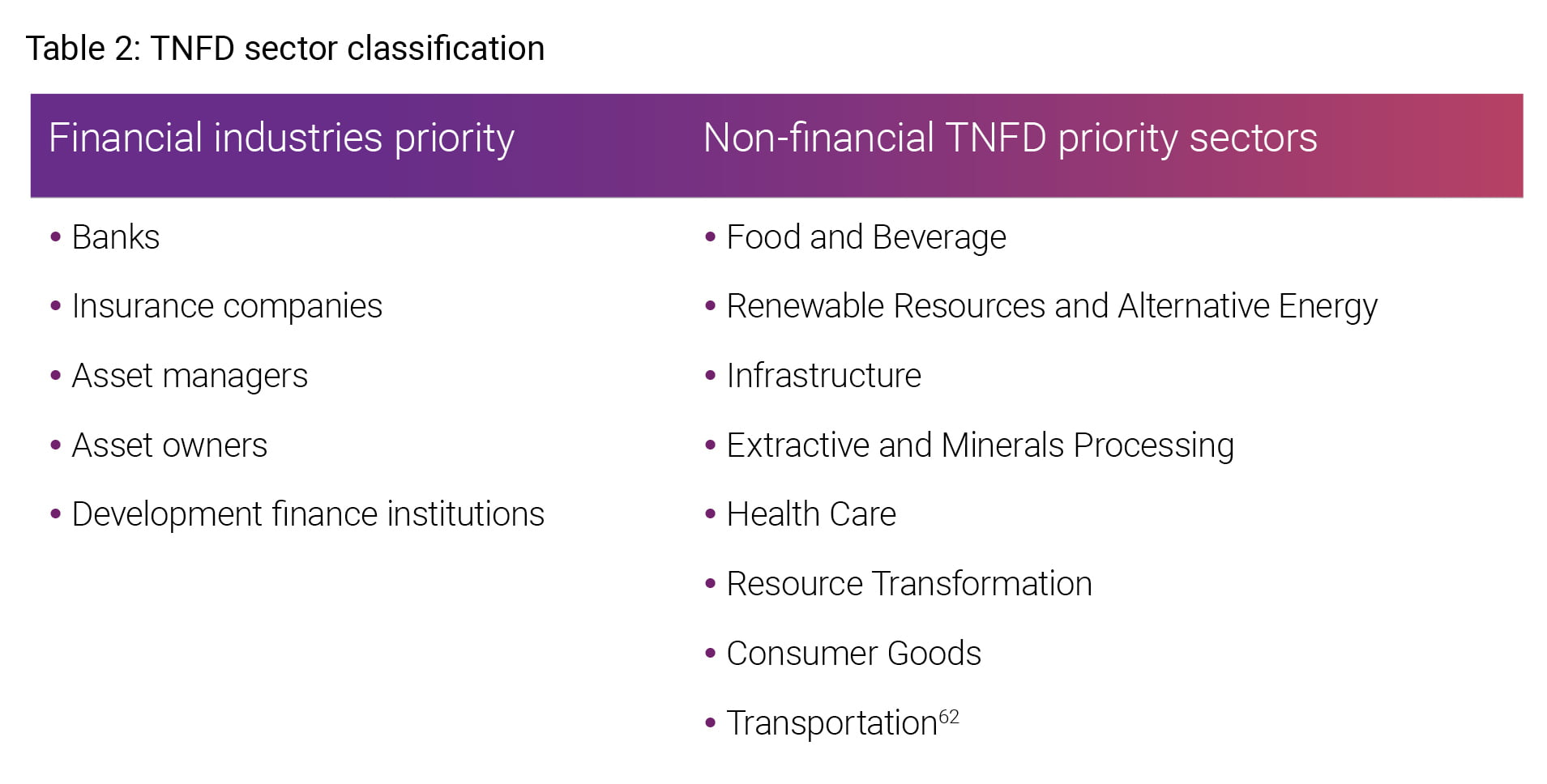

Beta versions of the framework have explored a general sector agnostic approach, while developing, ‘sector classification based on the Sustainable Industry Classification System (SICS).’ 61 Proposed priority sectors and industries for development of sector-specific guidance include [table above right],

Other nature frameworks

In addition to the TNFD Framework, there are many more. These include,

the Natural Capital Protocol, owned by the Capitals Coalition, released in 2016.63

the Corporate Ecosystems Valuation (CEV) (published in 2011) from the World Business Council for Sustainable Development (WBCSD).64

the GRI standard 304 Biodiversity from the Global Reporting Initiative (GRI). The GRI 304 Biodiversity standard is currently under review, and a revised standard is due in 2023.65

For a case study of natural accounting in practice, download a copy of the CIMA Academic report, ‘Natural Capital Accounting: Revisiting the Elephant in the Boardroom’.66

Future regulation and standards

European Corporate Sustainability Reporting Directive (CSRD)

Within the European Union (EU), the Corporate Sustainability Reporting Directive (CSRD) will replace the Non-Financial Reporting Directive (NFRD) in 2023. In April 2022, the European Financial Reporting Advisory Group (EFRAG) issued 13 exposure draft standards for public consultation. Once updated after the public consultation, the resulting drafts will be handed over to the European Commission to be considered for adoption as EU Sustainability Reporting Standards (ESRS).67

Within the five environment exposure drafts, ‘ESRS E4 Biodiversity & Ecosystems’ provides insight into future mandatory reporting standards on nature. It is clear from the ESRS E4 exposure draft that the ambition for reporting organisations is to focus their strategies and business models that are, ‘compatible with the transition to achieve no net loss by 2030, net gain from 2030 and full recovery by 2050.’68 Reporting organisations will be expected to describe their nature transition plans and policies addressing,

material biodiversity and ecosystems-related impacts;

its contribution to material biodiversity loss drivers;

material dependencies and material physical and transition risks and opportunities;

biodiversity friendly production, consumption and sourcing of raw materials;

screening and engaging with suppliers on biodiversity and ecosystems;

the social consequences of biodiversity and ecosystems related dependencies and impacts.69

Disclosure on targets and metrics focus upon an organisation’s transition plans (both mitigation and adaptation), and actions/activity to achieve no net loss by 2030, net gain from 2030 and full recovery by 2050. In the proposed reporting standard, the double materiality principle is at play in an organisation’s assessment. An organisation will have to disclose biodiversity and ecosystem factors where they materially impact the entity’s value. But also disclose where an organisation impacts biodiversity and ecosystem factors.

It is also important to beware that nature issues will feed across the four other environment ESRSs. For a comprehensive overview, it is worth exploring the thread of biodiversity loss and degradation across,

ESRS E1 — Climate change70

ESRS E2 — Pollution71

ESRS E3 — Water and marine resources72

ESRS E5 — Resource use and circular economy73

IFRS Foundation’s International Sustainability Standards Board (ISSB)

The International Financial Reporting Standards (IFRS) Foundation Trustees created the Sustainability Standards Board (ISSB) in November 2021. Its remit is:

to deliver a comprehensive global baseline of sustainability-related disclosure standards that provide investors and other capital market participants with information about companies’ sustainability-related risks and opportunities to help them make informed decisions.

The ISSB is using a building block approach to developing sustainability standards. In March 2022, the first two exposure draft sustainability standards were released for consultation. These were,

IFRS S1 — General Requirements for Disclosure of Sustainability-related Financial Information

IFRS S2 — Climate-related Disclosures.

In early 2023, the ISSB will consult on future priorities. It is expected there will be a priority for the development of an exposure draft sustainability standard on nature and biodiversity. This is likely to focus on the disclosure of material information about significant nature and biodiversity-related risks and opportunities, and incorporate TNFD recommendations.

Regulatory requirements for nature targets and nature-related disclosure

As already detailed in the ‘What is accounting for nature’ section regulators and governments are progressively focused on the topic of nature and biodiversity loss, so increased legislation and reporting will affect organisations over the next five years. Time to build your accounting for nature literacy and experiment with ways of reporting internally, within organisations.

With respect to reporting, the reality is, even if you are not measuring and reporting on your organisation’s accounting for nature impact, somebody else is. Bodies and stakeholders use your exhaust data to benchmark your organisation’s sustainability performance and test the robustness of your strategy. Exhaust data is simply the digital trail of ‘breadcrumbs’ organisations leave, that stakeholders can then hoover up to increase their understanding of an entity’s natural capital performance and long-term viability. In April 2022, the Global Benchmarking Alliance announced its intention, through a nature benchmark methodology, to rank keystone companies on their efforts the protect the environment and its biodiversity.74

Building business resilience

Organisations that have already built their nature literacy and are further on their ESG (Environmental protection, Social inclusion, and Governance) journeys are proving to be more resilient businesses. During the first wave of the Covid pandemic in 2020, Linda Eling-Lee, the global head of ESG research at MSCI, notes that, ‘companies with high ESG rankings have outperformed rivals during the crisis’.75

A possible reason for this is the greater corporate adaptability that ESG reporting, and scrutiny provides organisations to rethink their business models in time of stress. A focus on accounting for nature and transitioning to nature-positive organisations can only help to strengthen their long-term resilience.

By building an organisation’s journey to becoming nature positive, based on science-based targets, the Science Based Targets Network believes the shift allows businesses to:

get ahead of regulation and policy changes.

strengthen their reputation among consumers, employees and society.

increase confidence of their investors, parent companies, and other stakeholders.

catalyze innovation that’s good for the planet, and for business.

open opportunities to collaborate with other stakeholders, including those in their corporate value chain, in the landscapes where they operate or source, and in their sector.

improve their medium-to-long-term profitability.76