Crisis management is one of the reasons organisations need high-level strategic oversight.

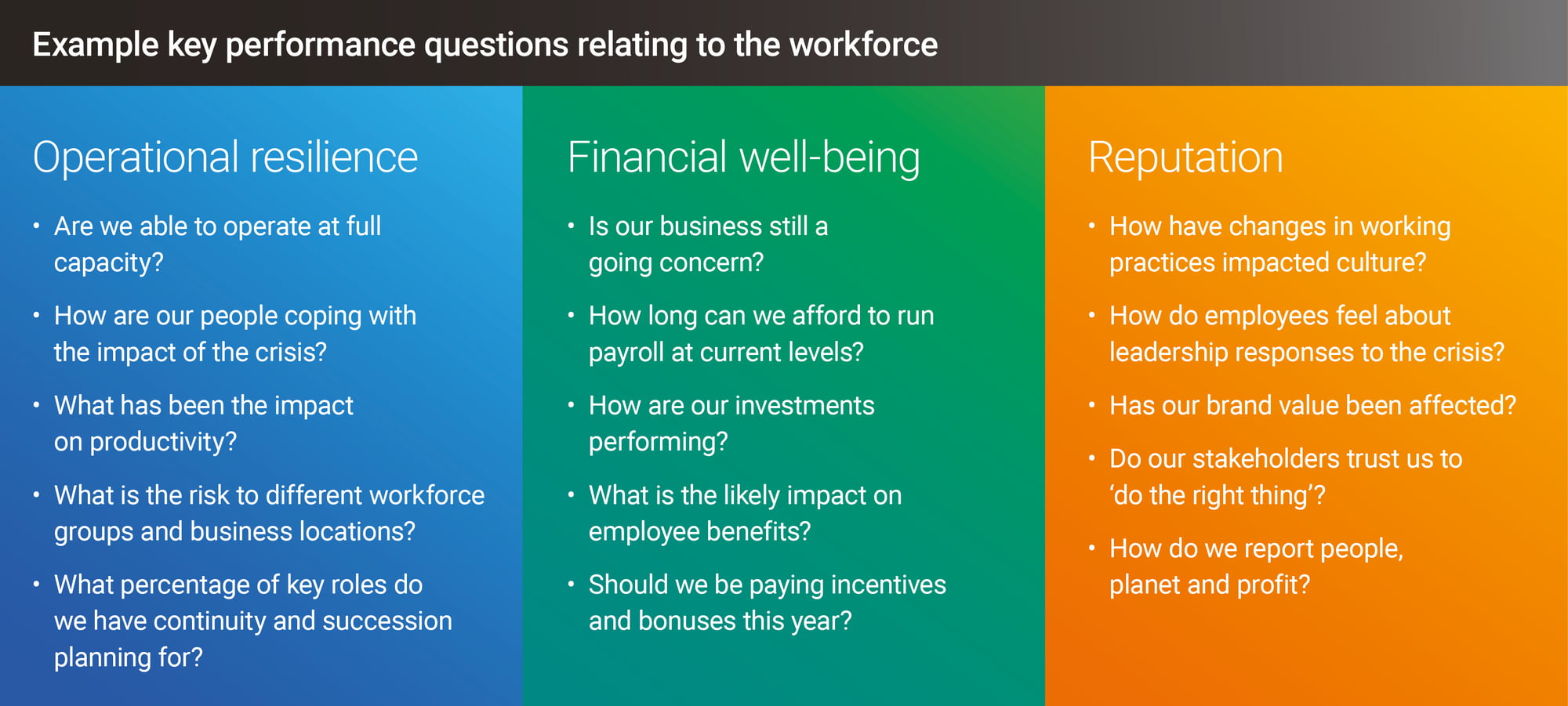

When things go seriously wrong in the organisational ecosystem, boards and executive committees focus on the organisation’s viability, looking at operational resilience, financial well-being and reputation.

To do this, they need good communication and clear information, both financial and non-financial. A defining characteristic of the COVID-19 pandemic has been the huge amount of advice and guidance by government, business, the media, scientists, health professionals and well-meaning individuals generate and share.

Even discounting the “fake news” so prevalent in today’s social media, there is so much “genuine” information flying around that it’s often hard to recognise what is relevant, and what really matters.

There is often far too much bumph in committee papers[i]. But with travel and social distancing restrictions indicating that business meetings will be held remotely for the foreseeable future, it’s more important than ever to cut to the chase. This will not be achieved by exception reporting or, at the other end of the scale, an endless list of red, amber and green KPIs. Indeed, the calculations behind our existing metrics may no longer be fair or appropriate.

In a complex world, there will be uncertainty around any decision. Management accounting systems and accounting figures should help to raise the right questions about what cannot be measured, rather than providing reassuring but faulty or irrelevant numerical answers.

‘Dealing with the Unknown’, CIMA 2016

[i] ‘Performance Reporting to Boards’, CIMA 2003

To understand the long-term impact of any disruption, the focus needs to be upon KPQs — the key performance questions that need answering around operational resilience, financial well-being and reputation. From this, we can identify the KPIs that will address and answer these questions[i].

[i] ‘How to develop non-financial KPIs’, CGMA 2012

Although it may be tempting to analyse past actions, committee discussions should also look forward. There will be increased demand for forward-thinking analytics that deliver the insight needed for strategic decision-making.

In the current situation, there will be statutory reporting implications to consider, including going concern conditions, principal risks and uncertainties and adjusting events. Unlike the majority of business crises, the COVID-19 pandemic has posed a direct threat to every employee, customer, supplier, investor. And with their families also under threat, there is more at stake than there has ever been.

In this context, and with growing interest in the reporting of non-financial assets, driven largely by the sustainability agenda, boards must consider the ways in which, and how effectively, they will report their People metrics to investors.