What are the requirements for ESRS and the CSRD?

The EU CSRD regulation requires companies to report on sustainability issues based upon 12 ESRS. These ESRS specify the information an organisation must disclose about its ‘material impacts, risks and opportunities in relation to environment, social, and governance sustainability matters’.5

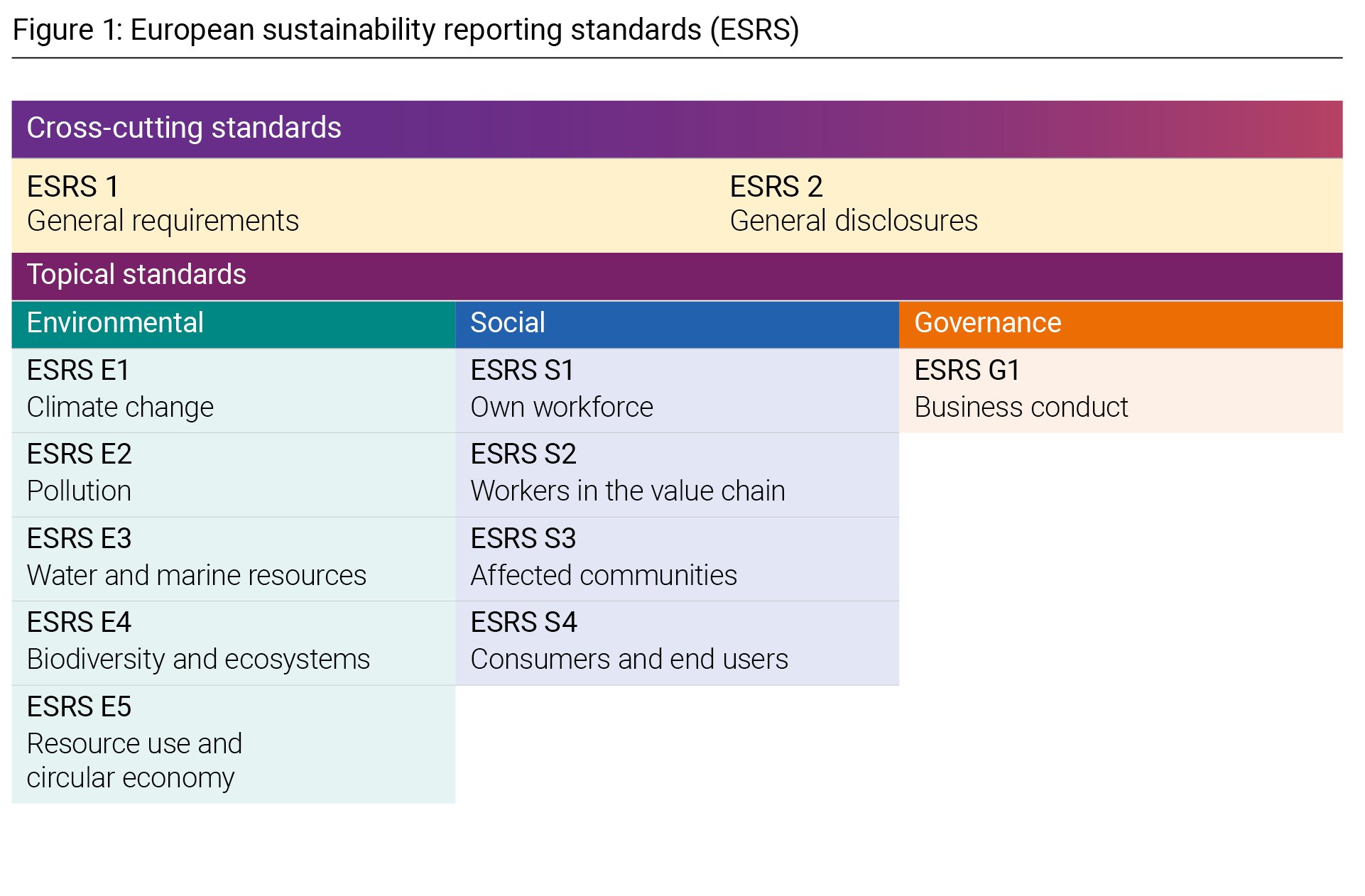

There are three categories of ESRS standards:

Cross-cutting standards (2)

Topic standards

Environmental (5)

Social (4)

Governance (1)

Sector-specific standards (coming later)

The resulting organisational disclosures in the form of a ‘sustainability statement’ also provide insights into a company’s:

Sustainability strategy, targets and progress.

Products and services.

Incentive programmes.

Business relationships and full value chain.

ESRS 1 General requirements

ESRS 1 ‘describes the architecture of ESRS standards, explains drafting conventions and fundamental concepts, and sets out general requirements for preparing and presenting sustainability-related information’.6

The standard sets out:

Qualitative characteristics.

Double materiality.

Sustainability due diligence.

Value chain (upstream and downstream).

Time horizons.

Preparation and presentation.

Structure of sustainability statements.

Linkages with other parts of corporate reporting and connected information.

Transitional provisions.

ESRS 2 General disclosures

ESRS 2 ‘establishes Disclosure Requirements on the information that the undertaking shall provide at a general level across all material sustainability matters on the reporting areas governance, strategy, impact, risk and opportunity management, and metrics and targets’.7

A four-pillar approach aligns with international sustainability reporting frameworks such as the Task Force on Climate-Related Financial Disclosure (TCFD) and Task Force on Nature-Related Financial Disclosure (TNFD). The four pillars are as follows:

Governance: ‘The governance processes, controls and procedures used to monitor, manage and oversee impacts, risks and opportunities’. (ESRS 2, chapter 2)8

Strategy: ‘How the undertaking’s strategy and business model interact with its material impacts, risks and opportunities, including how the undertaking addresses those impacts, risks and opportunities’. (ESRS 2, chapter 3)9

Impact, risk and opportunity management: Processes that ‘(i) identify impacts, risks and opportunities and assess their materiality’ (ESRS 2, chapter 4, section 4.1), and ‘(ii) manage material sustainability matters through policies and actions’. (ESRS 2, chapter 4, section 4.2)10

Metrics and targets: ‘The undertaking’s performance, including targets it has set and progress towards meeting them’. (ESRS 2, chapter 5)11

Topical ESRS

These 10 ESRS cover a range of sustainability topics that ‘can include specific requirements that complement the general level Disclosure Requirements of ESRS 2’.12 Topical ESRS follow the four-pillar approach structure and have similar objectives.

The objective across the 10 ESRS are to specify disclosure requirements, which enables users of the sustainability statements to understand the following:

Impacts – How an organisation affects the topic, in terms of material positive and negative actual and potential impacts.

Actions – Any actions taken, and the result of such actions, to prevent or mitigate actual or potential negative impacts and to address risks and opportunities.

Business model – The plans and capacity of the undertaking to adapt its strategy and business model, in line with the transition to a sustainable economy, and with the need to prevent, control and limit the topic issues.

Dependencies – The nature, type and extent of the undertaking’s material risks, dependencies and opportunities related to the topic and how the undertaking manages them.

Financial effects – The financial effects on the undertaking over the short-, medium- and long-term of material risks and opportunities arising from the undertaking’s topic-related impacts and dependencies.