From the management accountant’s perspective, a shared understanding of the business model and the strategic objectives for its development provide a basis for determining the appropriate measures to be used in the management of operational performance and progress towards strategic objectives.

Long-term value creation is a greater challenge than meeting this year’s budget. Achieving both at the same time requires more advanced performance management than can be achieved using financial measures alone. It involves managing both how the business is performing and how it is transforming.

Intangibles are often the main drivers of value and long-term success. These include the value proposition, customer satisfaction, brand recognition, supplier relationships, staff engagement, and other qualitative aspects of the business model.

But the first intangible on which all others are built is the quality of decision-making, including performance management. This is management accounting’s domain. Effective decision-making is measured and rational. It is based on relevant information, analysed with a focus on the value to the business and it is applied to achieve impact.

The measures used in performance management should be consistent with the business’ vision and strategy. Ideally, they should be leading measures with causal linkages to intended outcomes. Causality is seldom linear, so the measures selected have to be reviewed.

Determining which measures to use requires an ongoing dialogue to continually refine a shared vision of how the business works. Leaders’ articulation of the business model and its direction provides an opportunity to reconsider the measures to use.

New big data sources of non-financial data should be considered for measures or descriptors of intangibles. Management accountants may not be expected to conduct advanced analytics, but they should be alert to the data sources available and how that data could be analysed.

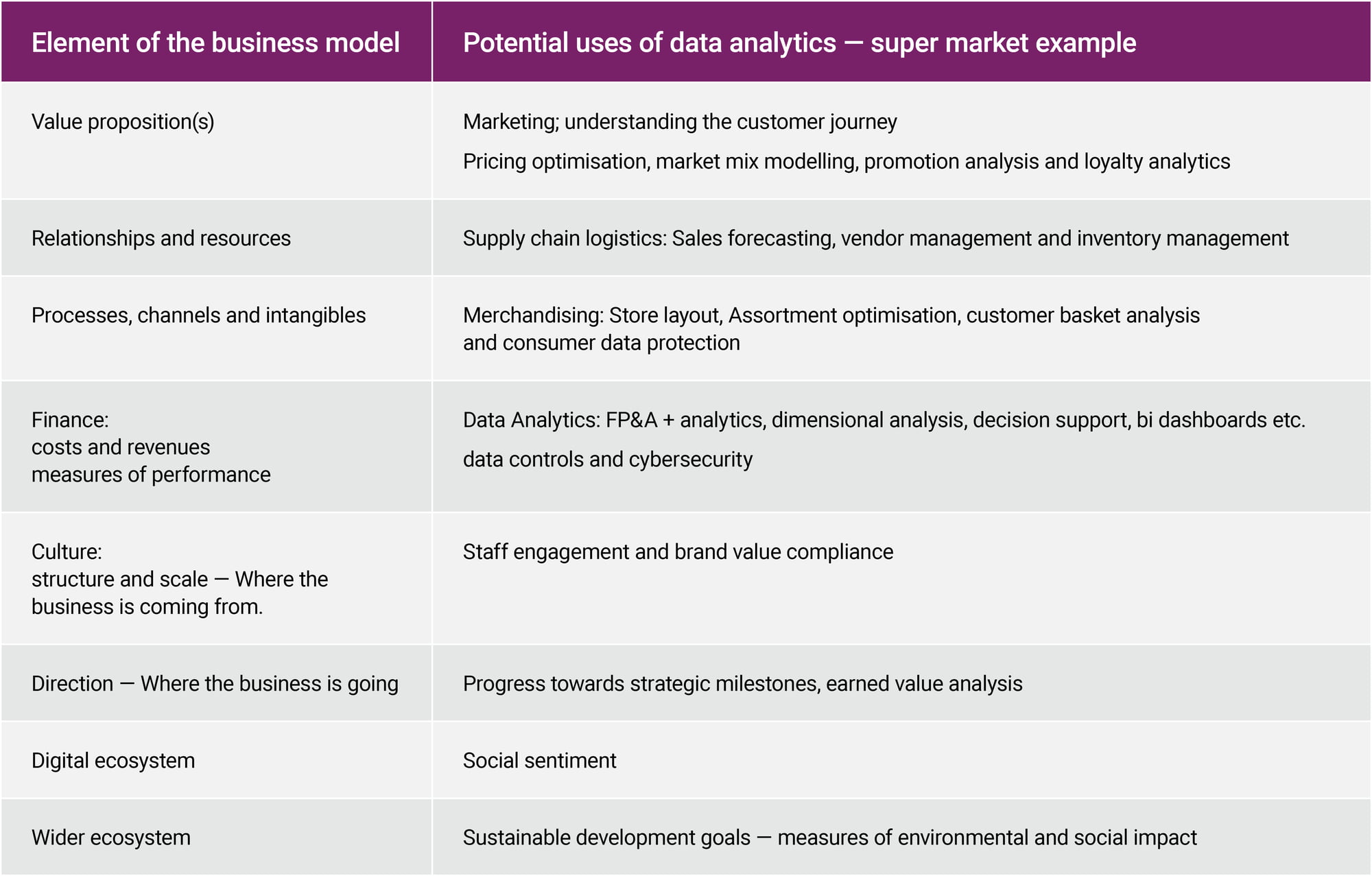

This table provides examples of how data analytics is used by supermarkets:

Research shows that the organisations with the best prospects of emerging successfully from a recession balance cutting costs to improve operating efficiency while investing in their competitive position.18

It may be unwise to defer investing in information technology to save costs:

Better analytics could provide insights into how to manage and improve performance.

Technology can save costs by automating routine tasks or even by automating some decision-making.

Technology can enable agility by providing scalability and the flexibility to relocate activities.

Management accountants should be alert to the use cases for new technologies and be prepared to assess the case for investments that might ensure the business’ long-term prospects.

18 Roaring out of Recession, Gulati, Nohria and Wohlgezogen, Harvard Business Review, March 2010

Businesses need to become agile so that they can anticipate and respond to the changes ahead. They must also continue to manage how the current business generates value.

A twin-track approach can be taken to ensure that business as usual continues to be managed effectively while innovations or new strategies are also developed and implemented by empowered, agile teams.

New ventures into the unknown are risky. It is important not to bet the farm on unproven initiatives. Agile teams are empowered to get things done. They work closely with customers to ensure their needs are addressed, experiment on a small scale at a low cost, adapt iteratively and prepare to cut losses and learn lessons if stage gates are not met. Essentially, ‘agile’ is about developing a culture where the management and control cycle is speeded up. Management accountants engaged in the management control cycle contribute professional objectivity and skepticism; accounting subject matter expertise and business understanding; questioning and analytical skills and the communication skills needed to engage with others to get things done.