Setting a transaction’s history in stone

A blockchain is a distributed ledger that digitally records the full history of a transaction. It stores this information in ‘blocks’ of data that are linked — or ‘chained’ — together. At its simplest, a blockchain is a database — one that’s shared or distributed among participants so that all can confirm, maintain and see the same record of events in close to real time. Encryption, digital signatures and protocols provide security. Each new data block or transaction record added to a chain is unique, date stamped and encrypted.

A blockchain is a type of database that takes a number of records and puts them in a block (rather like collating them on to a single sheet of paper). Each block is then ‘chained’ to the next block, using a cryptographic signature. This allows blockchains to be used like a ledger, which can be shared and corroborated by anyone with the appropriate permissions.

Distributed Ledger Technology: beyond blockchain, UK Government Office for Science, 2016

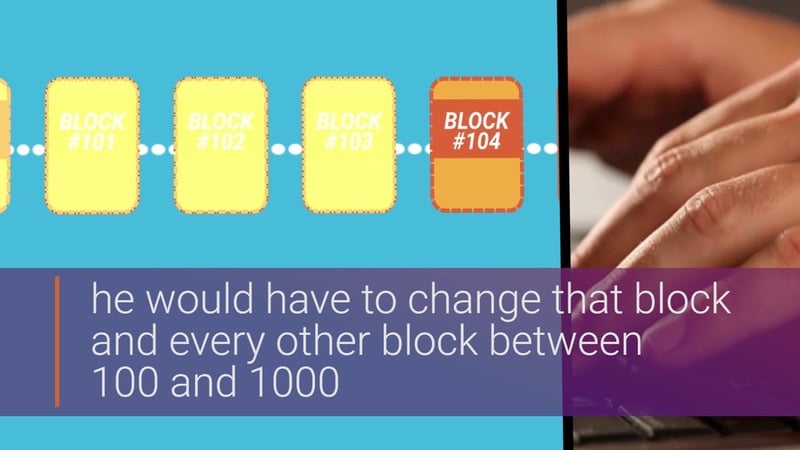

All the participants’ computers act as nodes to authenticate and confirm the validity of each new transaction (or ‘block’) as it is added to the chain. This consensus-based verification makes entries almost impossible to change — in fact, historic records are unalterable unless a pre-agreed protocol (such as a majority decision) allows amendments. You can also create smart contracts by embedding program code in a block of the chain to define a contractual term and carry out a pre-agreed instruction. This might authorise an automatic payment once a contractual condition has been met, following the delivery of goods or the completion of a service.